Money Monday

3 THINGS THAT CHANGED YOUR MONEY THIS WEEK

You may not have followed the markets last week but your money definitely did.

Watch Crystal`s full breakdown and understand what these developments mean in plain English.

Which matters most to your pocket: the Naira, oil prices, or the CBN`s liquidity move?

Tell us in the comments.

Follow Marina Times every Monday for your weekly money update.

#moneyupdate #nigeriaeconomy #naira #exchangerate #oilprices #cbn #omo #financialmarkets #investing #financialliteracy #businessnews #nigeriafinance #moneymatters #marinatimes

ESG CORNER

ESG is no longer about what companies promise. It’s about what they can prove.

The second half of 2026 is ushering in a new era of sustainability one where capital, regulators, and businesses are rewarding execution over rhetoric.

From Nigeria’s growing ESG ecosystem to global investments in renewable energy, sustainable aviation fuel, carbon removal, and low-carbon materials, the focus is shifting toward tangible infrastructure and measurable outcomes.

The message for businesses is simple:

ESG is no longer a communications exercise. It is becoming an operational requirement.

Do you think companies are finally moving from ESG promises to real action? Tap link in bio to read more.

Like, comment your thoughts, and follow Marina Times NG for more ESG, business, and market insights.

#esg #sustainability #climatefinance #greenfinance #nigeriabusiness #sustainablebusiness #climateaction #esginvesting #transitionfinance #corporatesustainability #africabusiness #marinatimes

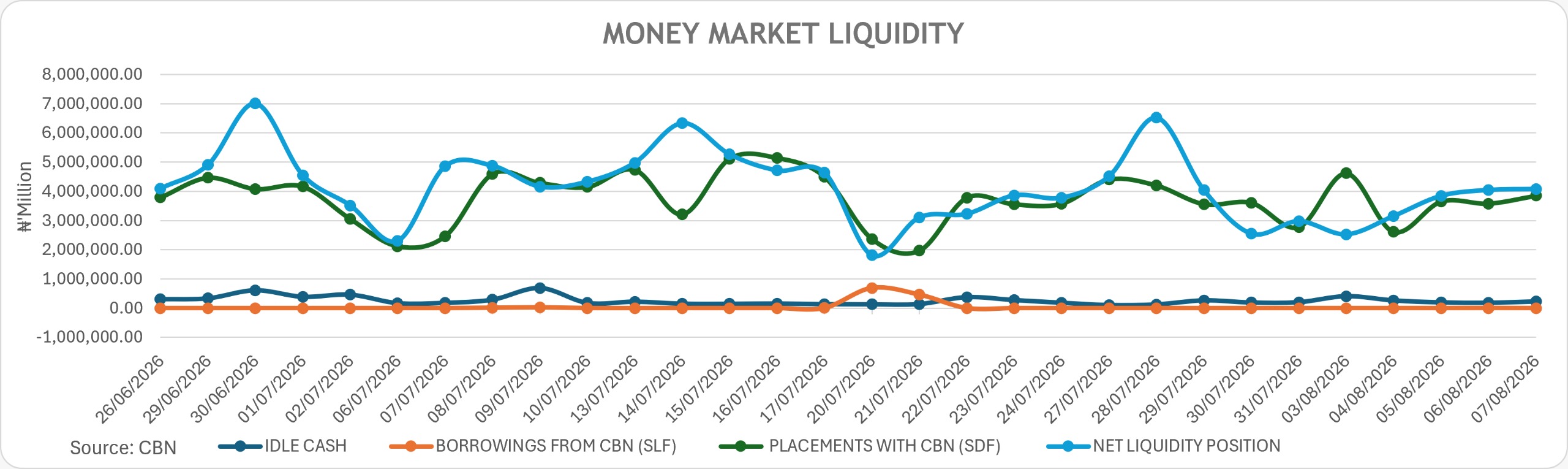

Weekly Market Review

Nigeria’s markets showed cautious optimism this week.

Liquidity surged to ₦4.08tn, the Naira remained stable at ₦1,365.69/$, while investors continued to favour attractive fixed-income yields.

Meanwhile, Nigeria unveiled a new tax framework for virtual assets, and global markets reacted to shifting rate expectations and geopolitical risks.

Swipe through for the key market developments and follow Marina Times for weekly financial insights. Tap link in bio to read more.

#nigeriamarkets #fixedincome #ngx #naira #financialmarkets #investing #nigeriaeconomy #capitalmarkets #virtualassets #financialnews #marinatimes

MARKET MYTH FRIDAY

Myth: "All cryptocurrencies are Bitcoin."

If you`ve ever called every cryptocurrency "Bitcoin," you`re not alone but they`re not the same.

Bitcoin may have been the first cryptocurrency, but today there are thousands of digital assets, each built for different purposes.

Before today, did you think all cryptocurrencies were Bitcoin?

Let us know in the comments.

📌 Save this post.

📤 Share it with someone interested in crypto.

Follow @MarinaTimesNG every Friday as we separate facts from finance fiction.

#bitcoins #cryptocurrency #blockchainbase #ethereumnews #stablecoins #digitalassets #cryptoeducation #financialliteracy #investing #cryptonews #finances #moneymatters #marinatimes

Part 4: Feeling is The Secret (Reality as the Shadow of Old Thinking)

Your current reality is not the full story. It’s the shadow of your former thoughts. Tap link in bio to read more.

#deepthoughts #growthmindset #resilience #personaldevelopment #lifelessons #mindsetmatters #overcomingchallenges #marinatimes

Marina Times Opinion

Nigeria is already one of the world`s largest digital asset markets.

The real question isn`t whether Nigerians will use cryptocurrencies it`s whether Nigeria will build the right regulatory framework to support them.

Inspired by Dubai`s Virtual Assets Regulatory Authority (VARA), this opinion explores why Nigeria should establish a dedicated regulator for digital assets one that promotes innovation while protecting investors, strengthening market integrity, and supporting financial inclusion.

Regulation doesn`t have to slow innovation it can be the foundation that allows it to thrive. Tap link in bio to read more.

Do you think Nigeria should create its own Virtual Assets Regulatory Authority? Tell us in tthe comments

Like this post, share your thoughts below, and follow Marina Times NG for more insights on digital assets, regulation, and financial markets.

#nigerian #vara #digitalassets #cryptocurrencynews #blockchainnews #stablecoins #fintech #africafinance #financialinnovation #cryptoregulation #digitaleconomy #marinatimes

Alternative Asset Update

Successful trading isn`t about guessing it`s about reading the market.

Every price chart tells a story, and technical analysis helps traders understand that story through patterns, trends, and market behaviour instead of emotions.

Remember, no single indicator guarantees success. The best traders combine multiple tools with disciplined risk management to make informed decisions.

Which technical analysis tool do you use the most candlestick patterns or support and resistance? Tap link in bio to read more.

Like this post, share your thoughts below, and follow Marina Times NG for more crypto, trading, and investment education.

#technicalanalysis #tradingsignals #candlestickcharts #supportandresistance #cryptotrading #stockmarketinvesting #forexanalysis #investing #marinatimes

What is a Stablecoin?

It’s crypto that doesn’t swing like Bitcoin.

Most stablecoins are pegged 1:1 to the US Dollar basically a digital dollar you can use on the internet.

People use them to:

✅ Send money across borders fast

✅ Protect their money from volatility

✅ Trade other crypto

✅ Make online payments & save

Simple. Stable. Useful.

Follow @marinatimes for more money talk

#stablecoin #cryptoexplained #digitaldollar #usdt #usdc #cryptonigeria #fintech #marinatimes #moneymatters #cryptoeducation

Legal Insights

Your National Identification Number (NIN) is no longer just an ID it`s becoming the key to participating in Nigeria`s digital economy.

The new NIMC Act 2026 expands identity registration, strengthens digital verification, and makes NIN a mandatory requirement for accessing critical services, from banking and SIM registration to business registration and government services.

The Act also aims to improve financial inclusion, reduce identity fraud, strengthen credit assessment, and create a more secure digital identity system for individuals and businesses.

As Nigeria`s digital economy grows, compliance with the new framework will become increasingly important for both citizens and organisations. Tap link in bio to read more.

Do you think the new NIMC Act will improve service delivery and strengthen Nigeria`s digital economy? Tell us in the comments.

Like this post, share your thoughts in the comments, and follow Marina Times NG for more legal, business, and economic insights.

#nimc #digitalidentity #nigerian #legalinsights #digitaleconomy #financialinclusion #dataprotection #businessplan #finances #publicpolicy #marinatimes

Every major AI company is spending at a pace rarely seen in modern technology.

Billions are flowing into GPUs, data centers, electricity, talent, and increasingly sophisticated models. Yet many of these companies are still reporting thin margins or significant losses.

At first glance, it looks unsustainable.

But history tells us that transformative technologies often look expensive before they become indispensable.

The internet did (late 1990s).

Cloud computing did (mid-2000s).

Ride-hailing (2010s)

Even railroads and electricity required enormous upfront investment before delivering lasting economic value.

Today`s AI race is no different.

The challenge is that this isn`t just a race to build the smartest model. It`s a race to build a business that can consistently generate returns on unprecedented capital investment.

The winners will likely be those that can answer four critical questions:

• Can they reduce the cost of training and inference?

• Can they convert users into recurring revenue?

• Can they build products customers cannot easily replace?

• Can they achieve profitability before investor patience runs out?

As infrastructure improves, chip efficiency increases, and enterprise adoption accelerates, today`s cost curve may begin to flatten. But until then, the industry remains in a delicate balancing act between innovation and financial sustainability.

The question for investors, founders,

and policymakers is no longer whether AI will change the world.

It`s whether today`s level of spending will create tomorrow`s enduring businesses or become another lesson in the cost of technological exuberance.

Capital can fuel innovation.

Only sustainable economics can sustain it.

What do you think? Are we witnessing the birth of the next industrial revolution, or the early stages of an AI valuation reset?

#artificialintelligence #aiphoto #technologynews #innovations #investing #venturecapital #startups #businessstrategy #digitaltransformation #futureofwork #marinatimes

Why does everyone pay attention to S&P Global?

When S&P Global releases an economic report or changes a country`s outlook, global markets pay attention.

But what exactly is S&P Global, and why does it matter to businesses, policymakers, and financial markets? Swipe through to find out.

Had you heard of S&P Global before today? What surprised you the most?

Join the conversation below.

Follow Marina Times NG for simple, insightful breakdowns of finance, economics, and global markets.

##financialmarkets #creditratings #globaleconomy #economicoutlook #capitalmarkets #macroeconomics #finances #financialeducation #marketinsights #businessnews #marinatimes

OPEC + Oli Production= ?

Understanding the institutions behind the headlines helps you make sense of the markets before they move.

💬 How much do you know about OPEC? What surprised you the most?

Join the conversation below in the comments.

Follow Marina Times NG for simple, insightful breakdowns of finance, economics, and global markets.

#financialmarkets #creditratings #globaleconomy #economicoutlook #capitalmarkets #macroeconomics #finances #financialeducation #marketinsights #businessnews #marinatimes

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}