Artificial Intelligence (AI) may be the face of today’s technology revolution, but semiconductors are its nervous system, and lithography is the heartbeat powering it all.

From generative AI systems and autonomous vehicles to defence systems and hyperscale cloud infrastructure, the global AI boom is accelerating demand for increasingly advanced chips. At the centre of this transformation lies one of the world’s most complex manufacturing technologies: Extreme Ultraviolet (EUV) lithography.

The semiconductor industry is no longer just a technology sector. It has become a geopolitical asset class, a stock market catalyst, and a determinant of national economic power.

According to Gartner, global semiconductor revenue could exceed $1.3 trillion by 2026, representing one of the strongest industry expansions in decades. AI semiconductors alone are expected to contribute nearly 30% of industry revenue this year.

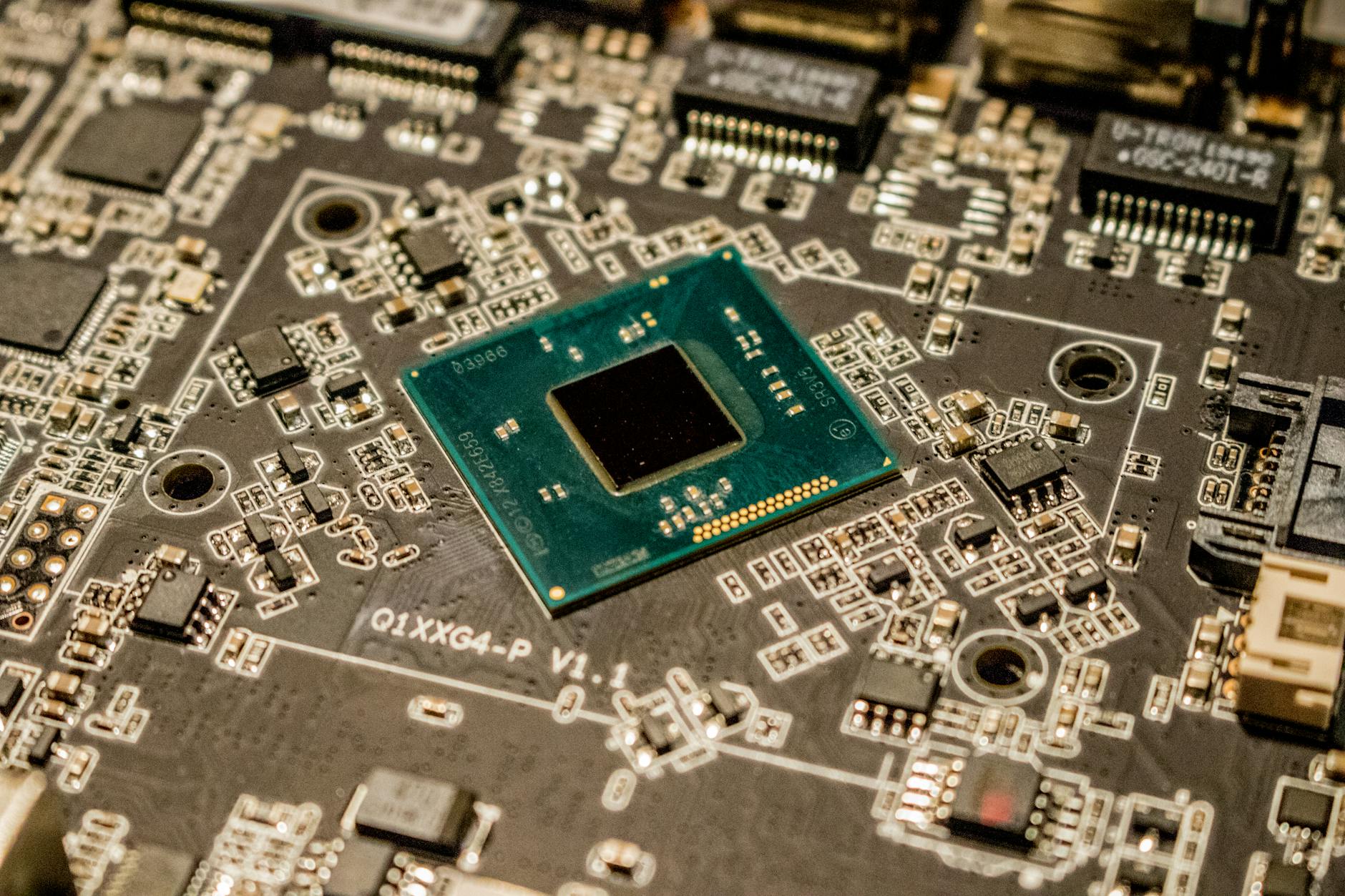

Lithography is the process of printing microscopic circuit patterns onto silicon wafers. The more advanced the lithography system, the smaller and more powerful the chip produced.

Modern AI models require enormous computational power, which depends on highly cutting-edge chips manufactured at 5nm, 3nm, and increasingly 2nm process nodes. Producing these chips is impossible without EUV lithography systems.

The Netherlands-based ASML N.V Holding company, dominates this market as the world’s only producer of commercial EUV lithography machines. Each machine is estimated to cost over $150 million and contains thousands of precision-engineered components.

Without ASML’s systems, companies like NVIDIA, TSMC, Samsung Electronics, and Intel would struggle to manufacture the advanced processors powering AI data centres today.

The rise of generative AI has fundamentally reshaped semiconductor demand dynamics.

Training large AI models requires thousands of Graphics Processing Units (GPUs) operating simultaneously in massive data centers. This has created extraordinary demand for high-performance AI accelerators, memory chips, advanced packaging technologies, and foundry capacity.

According to Deloitte’s 2026 Global Semiconductor Industry Outlook, the AI chip market is estimated to reach approximately $500 billion in 2026, while the broader semiconductor industry may approach $2 trillion annually within the next decade.

TrendForce projects global foundry revenue to grow nearly 25% in 2026, driven primarily by AI-related chip production.

The result is a historic capital expenditure cycle across the semiconductor supply chain.

The AI-driven semiconductor boom has triggered one of the strongest rallies in technology equities globally.

The Philadelphia Semiconductor Index (SOX), a major benchmark for chip stocks, has surged alongside rising AI infrastructure spending. Reuters reports that semiconductor stocks globally rallied after strong AI demand forecasts from AMD, while Asian semiconductor giants have emerged as major beneficiaries of the AI trade.

ASML N.V Holding also raised its 2026 outlook, forecasting a new semiconductor equipment “supercycle” driven by AI chip manufacturing demand.

Meanwhile, Taiwan Semiconductor Manufacturing Company (TSMC) continues to experience extraordinary growth as the primary manufacturer behind chips designed by NVIDIA, AMD, Apple, and several hyperscalers.

A recent market analysis highlighted that TSMC’s reported revenue growth was roughly 30% year-over-year in early 2026, with AI-related revenues expected to double by 2027.

These gains are not isolated corporate wins. They are increasingly influencing national stock exchanges and economic outlooks.

Taiwan represents the clearest example of semiconductor manufacturing translating into national economic influence.

TSMC controls the majority of advanced semiconductor foundry production globally and remains indispensable to the AI supply chain. The company manufactures chips for NVIDIA, Apple, AMD, Qualcomm, and several leading AI firms.

This dominance has transformed Taiwan into a strategic technology hub.

Reuters reports that Taiwan’s equity markets have gained significant momentum as demand for AI infrastructure boosts semiconductor exports and manufacturing activity. Coupled with the Taiwan Stock Exchange (TWSE) reportedly surpassed Canada’s equity market capitalization in late April 2026, to become the 𝐰𝐨𝐫𝐥𝐝’𝐬 𝐬𝐢𝐱𝐭𝐡-𝐥𝐚𝐫𝐠𝐞𝐬𝐭 𝐬𝐭𝐨𝐜𝐤 𝐦𝐚𝐫𝐤𝐞𝐭, with a total market capitalization exceeding 𝐔𝐒$4.47 𝐭𝐫𝐢𝐥𝐥𝐢𝐨𝐧.

The strategic importance of Taiwan’s semiconductor ecosystem has also intensified geopolitical tensions, particularly between the United States and China, as control over advanced chip production increasingly defines technological leadership.

South Korea has also become a major beneficiary of the AI-driven expansion of the semiconductor industry.

Companies such as SK Hynix and Samsung Electronics dominate the global memory chip market, especially High Bandwidth Memory (HBM), which is critical for AI workloads.

Reuters reported that Samsung’s market capitalization surpassed $1 trillion amid surging AI demand, while South Korea’s KOSPI index has gained momentum from semiconductor-driven earnings growth.

The country is now aggressively expanding investments in advanced fabrication plants and AI chip infrastructure to maintain its global competitiveness.

The Netherlands holds one of the most strategically important positions in global technology through ASML.

Despite its relatively small economy, the country controls the world’s most advanced lithography technology. ASML’s monopoly in EUV systems has effectively made the Netherlands a gatekeeper in the global semiconductor race.

Export restrictions on ASML’s advanced machines to China demonstrate how semiconductor manufacturing has evolved into an instrument of geopolitical influence and national security strategy.

The semiconductor industry is now central to economic policy worldwide.

The United States, China, Japan, South Korea, Taiwan, and the European Union are all deploying industrial policy frameworks, subsidies, and strategic investments to secure semiconductor independence.

This includes:

Even supporting industries such as photoresists, wafer manufacturing, and computational lithography are experiencing rapid growth.

The competition is no longer simply about consumer electronics. It is about economic sovereignty, military capability, and control of the future AI ecosystem.

Despite extraordinary growth projections, the semiconductor supercycle is not without risks.

The industry faces:

Deloitte warns that the industry has become heavily concentrated around AI demand, creating vulnerability should AI investment cycles slow unexpectedly.

Additionally, the concentration of advanced manufacturing capacity in Taiwan remains one of the world’s most significant geopolitical risks.

The AI revolution is ultimately a semiconductor revolution.

Behind every chatbot, autonomous system, recommendation engine, and AI model lies an increasingly sophisticated semiconductor ecosystem powered by lithography.

Countries that dominate semiconductor manufacturing are now shaping the next era of economic and technological leadership. Companies controlling lithography, advanced fabrication, memory production, and AI accelerators are becoming the defining industrial giants of the 21st century.

As AI adoption accelerates globally, semiconductor manufacturing is evolving from a technology industry into critical infrastructure for the modern world.

In this new economic order, silicon is no longer just a component.

It is power.

Tags: