Longevity, Resilience, and the Imperative to Mobilise Capital

Africa’s capital markets are no longer a question of existence, but of effectiveness.

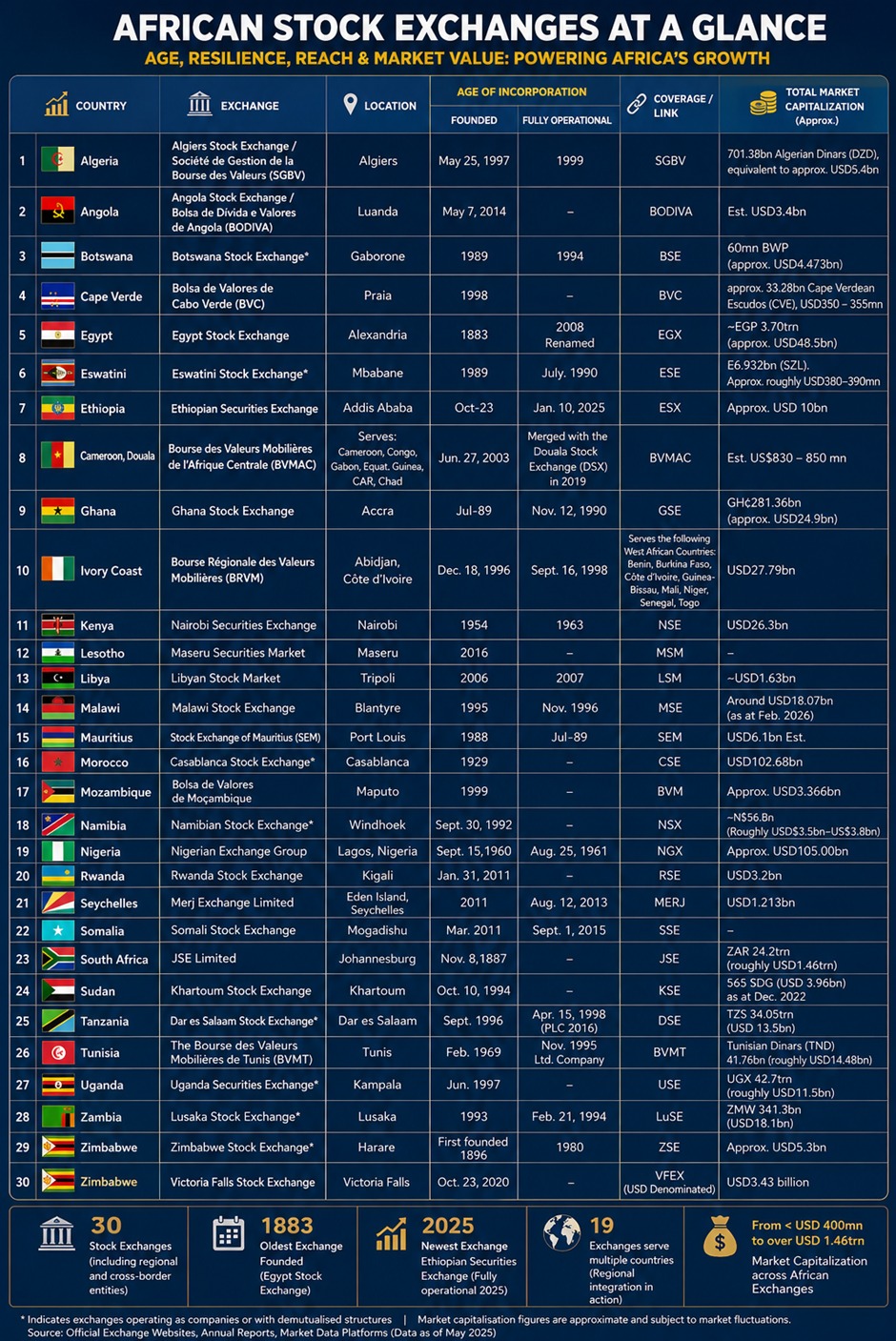

Across the continent, exchange incorporation spans generations. Some, like the Johannesburg Stock Exchange (founded 1887) and the Egyptian Stock Exchange (tracing roots to 1883), have operated for well over a century. Others, such as the Nigerian Exchange Group (1960) and the Nairobi Securities Exchange (1954), reflect post-independence financial institution building. More recently, markets like the Ethiopian Securities Exchange (launched in 2025) signal a new phase of expansion.

This longevity tells a powerful story: Africa’s capital markets are not new; they are resilient.

Yet resilience alone is no longer sufficient. The challenge now is whether these long-standing institutions can evolve into a connected, liquid, and growth-enabling system capable of financing the continent’s future.

Resilience Without Scale Is Not Enough

The age of Africa’s exchanges highlights endurance through political transitions, economic cycles, and structural reforms. However, longevity has not consistently translated into scale.

The Johannesburg Stock Exchange, with over a century of operation, stands as the continent’s dominant force, with a market capitalisation of approximately $1.48 trillion. In contrast, younger but significant markets such as the Nigerian Exchange Group (~$105 billion), the Casablanca Stock Exchange (~$102.6 billion, founded 1929), and the Ghana Stock Exchange (1989) remain comparatively smaller.

This divergence highlights a critical insight: time builds institutions, but not automatically depth or efficiency.

Fragmentation: A Persistent Structural Drag

Despite decades of operation, Africa’s capital markets remain largely disconnected.

Regional platforms such as the Bourse Régionale des Valeurs Mobilières (1996) and the Bourse des Valeurs Mobilières de l’Afrique Centrale (2003) demonstrate that integration is possible. However, most exchanges continue to operate within national boundaries, constrained by:

- Currency fragmentation

- Regulatory divergence

- Limited cross-border participation

The result is a continent rich in financial infrastructure, but poorly synchronised in capital mobilisation.

Liquidity: The True Test of Maturity

If longevity reflects resilience, liquidity reflects relevance.

Many African exchanges, despite decades of existence, still face low trading volumes, narrow investor bases, and limited institutional participation.

Markets such as the Nairobi Securities Exchange and the Ghana Stock Exchange illustrate this tension: established institutions with growing listings, yet constrained by intermittent liquidity.

Without active participation, even the oldest exchanges risk becoming repositories of value rather than engines of growth.

A New Generation of Markets, A New Opportunity

The emergence of newer exchanges introduces a different dynamic.

The Ethiopian Securities Exchange (ESE) represents a modern entry point, designed in an era shaped by digital finance and global capital mobility. Similarly, the MERJ Exchange Limited (2011) leverages technology to transcend geographic limitations, while the Victoria Falls Stock Exchange (2020) adopts a USD-denominated structure to mitigate currency risk.

These developments suggest that Africa’s next phase may not depend solely on legacy systems, but on how effectively old and new markets converge.

Nigeria: Bridging Legacy and Opportunity

Founded in 1960, the Nigerian Exchange Group embodies both history and potential.

As one of Africa’s most established exchanges, it has demonstrated resilience through economic cycles and policy shifts. Today, its role extends beyond national boundaries, it is positioned to act as a regional liquidity anchor for West Africa.

However, realising this potential will require: deeper institutional participation, enhanced liquidity frameworks, and stronger cross-border integration.

Nigeria’s trajectory will be vital in determining if longevity can translate into leadership.

The African Continental Free Trade Area (AfCFTA), the Eco, and the Future of Market Integration

Beyond domestic reforms, Africa’s broader integration agenda could become one of the most transformative forces for the continent’s capital markets. The AfCFTA, designed to deepen economic cooperation and facilitate cross-border trade, has implications that extend well beyond goods and services. Over time, its framework could support greater financial integration through harmonised regulations, improved investment mobility, and stronger interconnectivity between African exchanges.

Similarly, the proposed ECOWAS single currency, the ‘Eco’, although still facing implementation challenges, represents a potentially significant step toward reducing currency fragmentation within West Africa. A more unified monetary environment could lower transaction costs, improve cross-border settlement efficiency, and enhance investor confidence across regional markets.

If effectively implemented, these initiatives may help address one of Africa’s greatest structural limitations: the fragmentation of its financial markets. More importantly, they could accelerate the transition from isolated national exchanges toward a more connected continental capital market ecosystem capable of mobilising capital at scale and financing Africa’s long-term growth ambitions.

From Endurance to Effectiveness: A Continental Mandate

Africa’s capital markets have endured. The next step is transformation.

For policymakers: Longevity must be matched with reform, harmonised regulations, cross-border frameworks, and policies that unlock institutional capital.

For investors: The age of these markets signals stability. The opportunity lies in identifying where resilience meets growth potential.

For exchanges: The task is to evolve from standalone institutions into nodes within a connected continental system.

Conclusion: Time Has Built the Foundation, Action Must Build the Future

Africa’s capital markets are not starting from zero. They are built on decades, sometimes over a century, of institutional history.

That history is an asset that signals resilience, credibility, and continuity.

But the future will not be determined by how long these markets have existed.

It will be determined by how effectively they mobilise capital, integrate systems, and finance growth.

The objective is clear: Not just to sustain markets, but to make them work for Africa.

To invest in Africa today is to recognise both its history and its horizon, and to participate in shaping what comes next.

Disclaimer: Market capitalisation figures as of May 6, 2026, are approximate and subject to market fluctuations.