July 2026, Edition 1

Nigeria’s financial markets opened the second half of 2026 with a more delicate undertone, as elevated sovereign funding needs, a heavy Q3 issuance calendar and persistent bearish sentiment across fixed income and equities combined to keep investor conviction subdued. Although the system remains awash with liquidity and the Naira has shown relative stability alongside stronger external reserves, the scale of planned domestic borrowing has reinforced concerns about supply absorption, yield repricing and the continued crowding-out of private sector financing. At the same time, the FTSE Russell review delay, tighter regulatory action in the banking segment and fresh external financing support from multilaterals all point to a market still navigating the tension between reform progress and funding pressure, leaving investors increasingly tactical in an environment where liquidity is abundant, but risk appetite remains selective. Despite reduced Friday trading due to the US holiday in observance of Independence Day, commodities closed week-on-week (WoW) at pre-war levels, with Brent crude and West Texas Intermediate (WTI) at $72.07/bbl. (+0.10%) and $68.73/bbl. (-0.73%) respectively, while gold at $4,088.99/oz (+0.04%).

Interbank liquidity remained robust through the week, opening at ₦4.91 trillion, peaking at ₦7.00 trillion before closing at ₦ 2.87 trillion on Friday (-41.50% WTD). Money market rates were stable, with the Open Repo Rate (OPR) at 22.00% and the Overnight (O/N) rate at 22.18%. In the FX market, the Naira traded within a range of $/₦1,360.00 and $/₦1,390.00, before closing at $/₦1,370.19 on Friday.

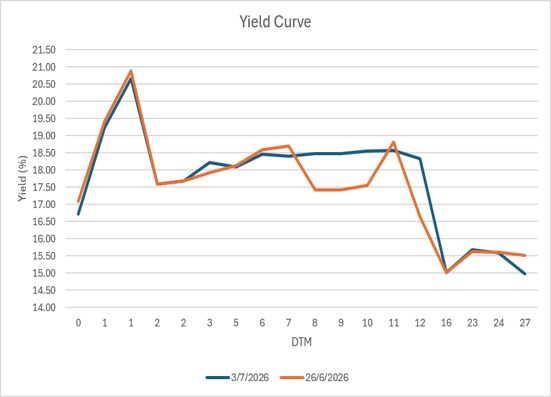

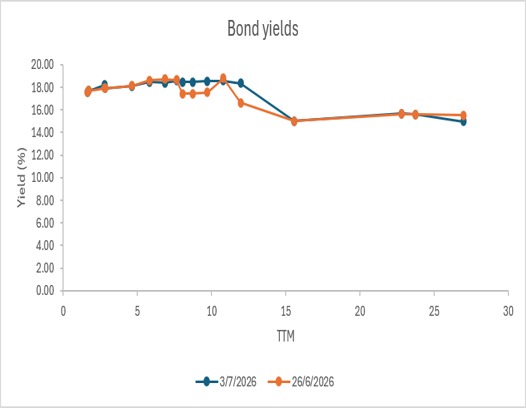

The fixed income market opened the week on a bearish note but recovered slightly with an average yield movement of 15bps for mid-tenor bonds during the period, as investors repositioned following the release of Q3, 2026 issuance calendar for Treasury bills and FGN bond. As a result, demand for the 2038s resurfaced with its re-introduction in the calendar. By Friday, bond yields declined from 19.00% to a lower-18.00% level for mid-tenors, while demand for the 2053s improved at the mid-15% level. Market participants locked horns in the OMO (Open Market Operations) space to capture approximately 21% yields in the money market, where rates largely held within the 19.85%–20.70% range, reflecting sustained demand for high-yield, short-term instruments. The 1-year Treasury bill rate also fell to the 17.00%-17.50% level at the close of the week, indicating ample liquidity conditions despite selective demand for the most recent Jun.-2027 bill.

FX Liquidity Pulse: The late June 2026 OMO auctions paint a clear picture of a deeply inverted yield curve, driven by a structural split in money market investor demand. Over the two-day session, the Central Bank of Nigeria (CBN) aggressively mopped up excess banking system liquidity, taking advantage of a 112.3% surge in day-two aggregate demand with total sale rising to ₦1.39 trillion from previous ₦0.947 trillion. Long-dated papers dominated investor appetite, with the 161-day bill drawing an overwhelming 6.05x oversubscription (₦1.18trn in bids), allowing the apex bank to compress long-end stop rates by 26bps to 19.80% from the earlier 9bps rise on the 134-day paper. Conversely, short-day demand forced a premium on the June 29 sale; the 22-day bill was undersubscribed at 0.58x, forcing the CBN to spike the stop rate by 31bps to 21.71% to clear the ₦174 billion sale, a trend that spilled into June 30 as the 7-day rate climbed an additional 19bps to peak at 21.90%. In all of this, the effective yield for these securities stood in the 21.00% band: 21.99%, 21.65% (+4bps), 21.99%, and 21.69% (+4bps) for the 22-, 134-, 7-, and 140-day bills, respectively.

AUCTION DATE | TENOR | OFFER (₦‘B) | BIDS (₦‘B) | TOTAL SALE (₦‘B) | STOP RATES (%) | PREVIOUS TENOR STOP RATES (%) |

| 22-DAY | 300.00 | 174.00 | 174.00 | 21.7100 | 20.4000 |

134-DAY | 300.00 | 873.00 | 873.00 | 20.0600 | 19.9900 | |

| 7-DAY | 300.00 | 409.00 | 409.00 | 21.9000 | 20.7100 |

161-DAY | 300.00 | 1183.50 | 990.00 | 19.8000 | 20.0600 |

Primary Issuance Brief: The Debt Management Office (DMO) and the CBN released the Q3 2026 issuance calendars for FGN Bonds and Nigerian Treasury Bills (NTBs), signalling a more aggressive domestic borrowing strategy. The FGN Bond calendar reflects increased issuance volumes, with July 2026 featuring three reopened issues: JAN 2035, APR 2037, and JUN 2038 (last issued in December 2024 at 16.50%), targeting a combined issuance of ₦1.40 trillion–₦1.70 trillion. For the remaining two months, the DMO plans to reopen only the 2035 and 2038 bonds, with issuance projected at ₦1.20 trillion –₦1.60 trillion each month, notably replacing the 2037 bond with the 2038 maturity. On the NTB side, the CBN has scheduled three auctions per month, up from the customary once every two weeks, with monthly maturities rising from ₦647.79 billion in July to ₦713.02 billion in August and over ₦1.28 trillion in September. New issuance will amount to ₦2.00 trillion and ₦2.10 trillion in July and August, individually, before easing by 19.05% to ₦1.70 trillion in September. Overall, the authorities plan to issue ₦5.80 trillion in NTBs against ₦2.64 trillion in maturities, highlighting a deliberate strategy to capitalise on ample system liquidity while addressing elevated government borrowing needs.

Effective July 1, 2026, the CBN, under Governor Olayemi Cardoso, revoked the operating licenses of 46 microfinance banks due to persistent regulatory violations and a failure to meet the minimum conditions required to operate. According to a statement by the acting Director of Corporate Communications, Mrs. Sidi-Ali Hakama, the action was executed under the Banks and Other Financial Institutions Act (BOFIA) 2020 after the banks committed severe infractions, including having insufficient assets to meet liabilities, shutting down operations without regulatory approval, prolonged inactivity, and failing to maintain unimpaired minimum capital. This sweeping measure is part of the CBN’s broader supervisory reforms to preserve the integrity and stability of Nigeria’s digital and financial ecosystems, safeguard public depositor funds from weak financial entities, while ensuring compliant, and healthy institutions continue to operate.

The Naira was relatively steady during the week in the Nigerian Foreign Exchange Market (NFEM), gaining ₦13.44 (-0.97%) week-to-date (WTD), and ₦10.74 (-0.78%) WoW, before closing at $/₦1,370.19 (WoW: ₦1,380.93). Foreign reserves increased to a record $51.46 billion (+0.41%) as of June 30, 2026, leading to a decline in blocked funds to $648.79 million (-1.72%) with a reduced blocked reserve ratio of 1.26% (-0.3bps), marking an improved foreign exchange condition despite external pressures.

The World Bank approved a $1.25 billion Development Policy Financing package for Nigeria in 2026, despite widespread public criticism over rising debt levels and transparency concerns, as part of a broader 2026–2032 Country Partnership Framework aimed at accelerating job creation, strengthening private sector–led growth, and expanding reforms in key sectors such as energy, digital infrastructure, agriculture, trade, and revenue mobilisation. The programme is designed to unlock investment, improve competitiveness, and support structural reforms, including deeper capital market development and regulatory modernisation, while also expanding access to electricity, broadband, and agricultural inputs. However, the approval comes amid ongoing public backlash over Nigeria’s growing external borrowing profile and fears of debt sustainability, making the loan both a financing and confidence signal for Nigeria’s reform agenda.

Nigeria made a notable diplomatic and energy-policy shift in 2026 by becoming the first OPEC member to join the International Energy Agency (IEA) as an associate member, a move that strengthens its integration into global energy governance while signalling closer cooperation between major oil producers and advanced energy economies. The decision, approved unanimously by the IEA Governing Board, expands the agency’s reach across countries representing over 80% of global energy demand and gives Nigeria access to enhanced data sharing, policy coordination, and energy transition frameworks, even as it remains a key producer of the Organisation of the Petroleum Exporting Countries (OPEC). Officials from both sides highlighted benefits such as improved energy security cooperation, investment visibility, and support for Nigeria’s domestic energy challenges, including electricity access and fuel system constraints, while the development is also seen as part of Nigeria’s broader strategy to balance its role within OPEC with engagement in global clean energy and transition-focused institutions.

The Nigerian Exchange (NGX) ended the week July 3, 2026, positive amid a broadly bearish run through the period, with the All-Share Index slipping from 228,401.92 points on Monday (June 29) to 229,240.34 points (WTD +0.37%, WoW -1.21%, and a year-to-date return of 47.31% down from 49.12%) by Friday. Trading activity weakened during the week, while market breadth improved marginally from 0.27x to a peak of 0.71x, remaining below 1.00x. Market capitalization trended below the ₦150.00trn mark during the week, as a brief midweek rebound, driven by a 10% rally in Airtel Africa, was quickly erased by heavy profit-taking in large-cap banking, industrial, and oil & gas stocks including Zenith Bank, GTCO, Dangote Cement, Aradel, FCMB, and First HoldCo, while sector performance weakened across the board with banking leading losses for most sessions and market breadth remaining negative despite intermittent spikes in turnover. With key structural development during the week, including:

For the week ended July 3, 2026, global financial markets navigated profound macro shifts interrupted by key central bank updates, major policy initiatives, and sharp currency swings. In Europe, newly confirmed figures showing a robust 0.6% expansion for the UK economy in early 2026 injected optimism into regional markets, while European Central Bank (ECB) President Christine Lagarde delivered an opening speech at the Sintra Forum highlighting the Eurozone’s enhanced structural resilience against external economic shocks. This optimism contrasted with developments in Asia, where the Japanese Yen plunged past ¥162 per dollar to hit a 40-year low, driven by the wide interest rate differential with the West and heavy currency hedging from foreign investors piling into Tokyo’s booming stock market. Capitalizing on the tech wave, South Korea’s President Lee Jae Myung unveiled a sweeping national investment plan alongside the CEOs of Samsung and SK Hynix, committing roughly $590 billion to construct the world’s largest AI semiconductor and packaging clusters. While this tech move initially induced volatility, dragging down South Korean chip heavyweights early in the week on fears of long-term oversupply, equities broadly rebounded by Friday. In the U.S., a cooler June nonfarm payrolls report showing just 57,000 jobs added alleviated near-term rate hike pressure from the Federal Reserve, propelling the Dow Jones Industrial Average to a new record high even as the broader tech sector experienced a rotation that left the Nasdaq mixed under selective profit-taking. Benchmark sovereign bond yields pared earlier gains during the holiday-thinned week, with the U.S. 10-year Treasury yield easing to close at 4.490% and the UK 10-year Gilt yield finishing slightly higher at 4.774%.

The equities market performance was positive, closing WoW at: the Nasdaq Composite at 25,832.67 (+2.10%), S&P 500 at 7,483.24 (+1.80%), and the blue-chip Dow Jones Industrial Average at 52,900.07 (+2.00%). Across Europe, Germany’s DAX 40 closed at 25,779.31 (+4.49%), while the FTSE 100 was at 10,679.03 (+1.63%), and the Stoxx 600 notched a fresh record high of 652.77 (+2.66%). Asian markets finished down, with Japan’s Nikkei 225 at 69,744.07 (+0.55%), China’s Shanghai Composite Index at 4,043.64 (+0.41%), Hong Kong’s Hang Seng Index at 23,350.03 (+2.99%), and South Korea’s KOSPI at 8,088.34 (-3.84%).

African markets reflected a mixed macro backdrop this week, with Ghana and Ethiopia highlighting both inflation volatility and reform resilience across the continent. In Ghana, inflation rose for the third straight month to 5.30% in June from 3.70% in May, pointing to a gradual re-emergence of price pressures after a period of sharp disinflation, though inflation remains well below the elevated levels seen in 2024. In contrast, Ethiopia received a further vote of confidence from the IMF, which completed the fifth review of the country’s 48-month Extended Credit Facility programme, unlocking about $464 million in additional financing and bringing total disbursements under the arrangement to roughly $2.65 billion. Together, the developments suggest that while inflation pressures remain uneven across African economies, continued reform progress and multilateral support are helping to anchor macroeconomic stability in key frontier markets.

The global commodities market for the week ended July 3, 2026, remained under sustained pressure as easing geopolitical risk in the Middle East and the gradual normalization of flows through the Strait of Hormuz drove crude prices back toward pre-conflict levels, with Brent slipping from about $74/bbl. at the start of the week to roughly $72/bbl. by Friday and WTI hovering near $69/bbl. The key theme was the market’s shift from war-risk pricing to oversupply concerns, as improving US-Iran diplomatic engagement, recovering Saudi and UAE exports, stronger Hormuz traffic, and additional Gulf supply all reinforced bearish sentiment despite still-elevated regional tensions. In contrast, gold strengthened steadily through the week, rising from around $4,020/oz to nearly $4,089/oz by July 3, supported by weaker-than-expected US labour data, reduced expectations for further Federal Reserve tightening, and softer oil prices that helped calm inflation fears while preserving safe-haven demand. Overall, the week reflected a clear divergence across commodities: oil retreated on improving supply and de-escalation signals, while gold advanced on a softer US rate outlook and renewed investor caution.

As Q3 opens, Nigeria’s financial markets are facing a difficult mix of heavy sovereign borrowing, sustained bearish sentiment across fixed income and equities, and abundant system liquidity, while the FTSE Russell review of Nigeria’s frontier market classification adds another layer of uncertainty for investors. The Federal Government’s strong funding appetite is coming at a time when markets are already digesting elevated supply, forcing both local and foreign investors to reassess portfolio strategy and where best to position for returns. July 2026 is expected to bring over ₦10 trillion in market inflows, driven by ₦352.44 billion in FGN bond coupons, ₦8.83 trillion in OMO maturities, ₦647.79 billion in NTB maturities, and US$78.42 million in Eurobond coupons. In the new week, the market is positioned for ₦2.21 trillion in OMO repayments, ₦269.36 billion in NTB maturities, and an NTB auction of ₦700.00 billion, with the offer split across the 91-, 182-, and 364-day bills in a 1:1:5 ratio. Together, these flows point to a liquidity-heavy market, but one where elevated sovereign issuance and cautious sentiment could keep investor positioning highly tactical.

By: Sandra A. Aghaizu

Loading…

Subscribe now to keep reading and get access to the full archive.