June 2026, Edition 5

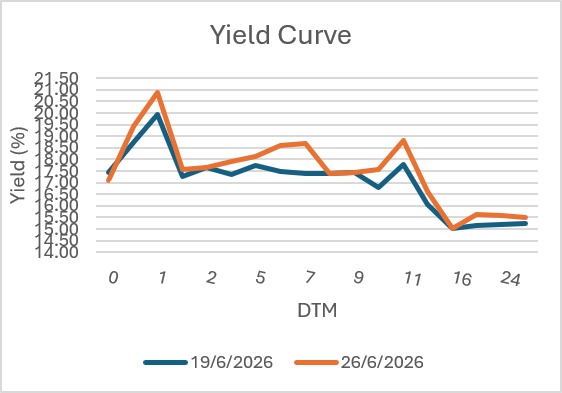

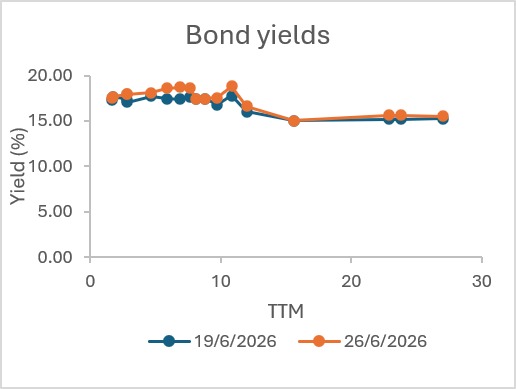

During the week ended June 26, 2026, yields traded higher as investors continued to navigate falling prices in Nigeria’s fixed-income market. Mid-tenor Federal Government of Nigeria [FGN] bonds breached 19%, while Open Market Operation (OMO) bills and Nigerian Treasury Bills [NTBs] sustained elevated rates within bands of 19.90%–21.75% and 17.00%–18.15%, respectively, reflecting persistent demand for short-term, high-yield instruments amid a higher-for-longer rate outlook.

Primary market activity from the Debt Management Office (DMO) and the Central Bank of Nigeria (CBN) remained strong, with robust oversubscriptions and higher stop rates reinforcing aggressive pricing dynamics, while secondary markets stayed selective, favouring mid-curve bonds at attractive yield levels. FX conditions were broadly volatile, with the Naira closing higher, supported by reserves rising above $51bn, while equities on the Nigerian Exchange weakened midweek on profit-taking, reversing early gains.

Globally, sentiment was pressured by hawkish US data and tech-led equity sell-offs, even as signals from the World Economic Forum Summer Davos 2026 reinforced a shift toward execution-driven growth narratives, leaving markets anchored on elevated yields and cautious risk appetite. Commodities closed low week-on-week (WoW), with Brent crude and West Texas Intermediate (WTI) at $71.90/bbl. (-10.67%) and $69.23/bbl. (-10.47%), respectively, while gold declined to $4,087.01/oz (-1.56%).

Interbank liquidity remained robust through the week, opening at ₦4.39trn, peaking at ₦6.14trn, before closing at ₦4.10trn on Friday (-6.69% WTD). Money market rates were stable, with the Open Repo Rate (OPR) at 22.00% and the Overnight (O/N) rate at 22.23% (-0.09bps). In the FX market, the naira traded within a range of $/₦1,365.50 and $/₦1,392.00, before closing at $/₦1,380.93 on Friday.

The fixed income market traded further bearish during the review period, as investors continued to reprice Treasury and OMO bills to higher yields, with FGN bonds responding to evolving yield expectations. By Friday, bond yields had breached 19% level for mid-tenors, rising from the 17% level at the beginning of the month. Activity was broadly spread across the money market, where levels largely held within the 19.90%–21.75% range, reflecting sustained demand for high-yield, short-term instruments. Treasury bill offers were within the 17.00%–18.15% band, indicating ample liquidity conditions despite selective bargain hunting. In the FGN bond market, trades were dominated by the 2035 and 2037 issues, with yields peaking as high as 19% from the mid-18% level where the week opened, while shorter-tenor papers such as the FGN Apr. 2029 and FGN Aug. 2030 also attracted steady interest. However, demand for the 2053s resurfaced with minimal interest. The market’s sustained bearish stance reflects heightened interest rate expectations, with investors’ appetite favouring a higher interest rate regime and strategic placements.

The June 2026 FGN Bond Auction, held at the week’s open by the DMO, featured two reopened papers: the 22.60% FGN JAN 2035 and 16.2499% FGN APR 2037. Both instruments witnessed strong demand of 1.18x, with allotments of 85.2% and 87.7%, respectively. Bid-to-cover ratios (BCR) stood at 1.17x and 1.14x, with clearing rates at 18.34% (+134bps) and 18.35% (+135bps), marking the highest single auction sales of the year, with total sales at ₦1.22tn (+1.825%). Amid the increase in stop rates into the 18% region, investors bid higher, raising the DMO’s borrowing cost while keeping issuance under control. It is also worth noting that there were no non-competitive bids, signalling active competitive participation by investors.

FGN Bond | 22.60% JAN 2035 | 16.2499% APR. 2032 |

Maturity Date | 29-01-2035 | 18-04-2037 |

Tenors | 10 | 20 |

Amount Offered (₦’B) | 600.00 | 600.00 |

Subscription (₦’B) | 705.22 | 708.27 |

Amount Allotted (₦’B) | 600.90 | 621.00 |

Stop Rates (%) | 18.3400 | 18.3500 |

Last Auction Stop Rates (%) | 17.0000 | 17.0400 |

Liquidity Pulse: The OMO auctions conducted between June 22 and 23, 2026, reflected sustained investor demand despite evolving yield dynamics. Demand remained concentrated in longer-dated tenors, with the 134-day and 140-day bills recording strong oversubscriptions of 6.84x and 5.21x, respectively, compared with 2.19x and 1.79x for the 99-day and 70-day maturities. While stop rates improved for the 99-day (+22bps), 134-day (+4bps), and 70-day (+35bps) bills, except for the 140-day (-3bps), effective yields remained broadly stable around 21.6%, suggesting balanced pricing conditions. Aggregate demand stood at ₦2.71 trillion on June 22 before moderating to ₦2.10 trillion on June 23, with the CBN allotting nearly all subscriptions (98.7% and 98.2%, respectively), highlighting its continued commitment to liquidity sterilisation. Overall, the auction outcomes point to persistent system liquidity, strong investor preference for duration, and a gradual pull toward the 21% region.

AUCTION DATE | TENOR | OFFER (₦‘B) | BIDS (₦‘B) | TOTAL SALE (₦‘B) | STOP RATES (%) | PREVIOUS TENOR STOP RATES (%) |

| 99-DAY | 300.00 | 658.00 | 658.00 | 20.4000 | 20.2800 |

134-DAY | 300.00 | 2,052.21 | 2,016.40 | 20.0200 | 19.9800 | |

| 70-DAY | 300.00 | 538.00 | 538.00 | 20.7500 | 20.4000 |

140-DAY | 300.00 | 1561.83 | 1524.83 | 19.9900 | 20.0200 |

Primary Issuance Brief: Total market participation remained strong across OMO bills, NTBs, and FGN bonds in H1 2026, with sustained oversubscription and robust liquidity absorption. In the OMO segment, total sales reached about ₦55.38trn, against ₦17.40trn offered and ₦66.31trn in demand, with ₦33.09trn sold in Q2 so far. Notably, June 2026 accounted for ₦11.61trn in sales against a ₦3.0trn offer, highlighting aggressive demand. In the NTB market, total issuance stood at ₦12.75trn offered against demand of ₦38.67trn, with ₦14.36trn sold in H1, while June alone recorded ₦2.95trn sold against ₦2.00trn offered and ₦4.02trn in demand, reflecting heightened short-term liquidity appetite. Meanwhile, FGN bonds recorded ₦4.95trn offered, ₦8.76trn in demand, and ₦5.08trn in total sales in H1, with June contributing about 24.01% of total sales, highlighting steady but more measured long-term investor participation.

The CBN data show that, despite a strictly maintained tight monetary policy stance keeping the benchmark interest rate at 26.50%, Nigeria’s broad money supply (M3) grew by 3.38% month-on-month to ₦129.21 trillion in May 2026, driven by an accumulation of both net foreign and domestic assets. According to the S&P Global report, Nigeria’s economic growth is experiencing a modest slowdown, with real GDP growth forecasts revised downward by 30 basis points to 3.7% for 2026 and 3.5% for 2027. This deceleration is primarily driven by persistent inflationary pressures, evidenced by a sharp upward revision in the 2026 inflation forecast to 16.9%, as a stronger-than-expected pass-through from global oil prices fuels domestic energy costs and dampens household consumption. Despite these mounting price pressures squeezing consumer purchasing power, broader economic growth is projected to remain resilient, anchored by higher domestic oil production and a stable exchange rate outlook.

The naira was volatile during the week in the Nigerian Foreign Exchange Market (NFEM), with a loss of ₦11.83 (+0.86%) week-to-date (WTD) and ₦10.48 (+0.76%) WoW, before closing at $/₦1,380.93, compared with $/₦1,370.46 WoW. Foreign reserves advanced above the $51bn mark to $51.25bn (+0.42%) as of June 25, 2026, leading to a corresponding decline in blocked funds to $660.16m (-1.72%), with an eased blocked reserve ratio of 1.29% (-0.3bps), signifying relatively stable foreign exchange conditions despite external pressures.

The Nigerian equities market experienced a volatile trading week, beginning with two consecutive sessions of gains before reversing sharply in the latter half. The NGX All-Share Index (NGXASI) rose on Monday at 238,219.19 to 240,743.19 on Tuesday, supported by a 10% surge in Airtel Africa and institutional bargain hunting in banking stocks (such as FIRSTHOLDCO, GTCO, ZENITHBANK, and FIDELITYBK), gaining 1.06% to add ₦1.64 trillion to the market cap. With investor sentiment and trading activity improving significantly.

However, the market erased these gains on Wednesday and Thursday as broad-based profit-taking intensified, led by heavy selloffs in industrial stocks, particularly DANGCEM and BUACEMENT, followed by sharp declines in oil and gas counters, including ARADEL and OANDO. Consequently, the NGXASI declined from 240,743.19 points at Tuesday’s close to 232,049.02 points (WTD -2.59%, WoW -1.65%) by Friday, with a reduced year-to-date return of 49.12% from 51.62%. Trading activity weakened in the second half of the week, while market breadth remained negative at 0.40x despite hitting a positive of 1.24x on Tuesday. Market capitalization (was volatile between the range of ₦151.84trn to ₦156.49trn during the week, reflecting cautious investor sentiment despite the early-week optimism.

Global financial markets experienced heightened volatility during the week ended June 26, 2026, driven by macroeconomic data and a strong sell-off in the technology sector. The key economic catalyst was Thursday’s U.S. Personal Consumption Expenditures (PCE) report for May, which revealed a hot 0.4% month-on-month increase that pushed the headline annual rate to 4.1% and the core reading to 3.4%, reinforcing the hawkish sentiment of the new Federal Reserve leadership under Chair Kevin Warsh, which is currently weighing rate hikes later this year.

This inflationary backdrop was compounded by an upward revision of Q1 U.S. GDP growth to an annualised 2.1% and robust nominal consumer spending (up 0.7%), which kept short-term sovereign bond yields elevated. The benchmark 10-year U.S. Treasury yield closed at 4.38% after hovering near 4.37% for much of Friday. Across the Atlantic, the UK 10-year gilt yield settled at 4.71%, holding near elevated levels as broader European markets navigated local fiscal dynamics.

Week-on-week (WoW), the equities market performance was mixed. At the WoW close, the tech-heavy Nasdaq Composite stood at 26,297.62 (-4.60%), the S&P 500 at 7,354.02 (-2.05%), and the blue-chip Dow Jones Industrial Average at 51,876.11 (+0.60%). Across Europe, Germany’s DAX 40 closed at 24,671.22 (-1.30%), while the FTSE 100 eased at 10,508.02 (+1.40%), and the Stoxx 600 defied the gloom to notch a fresh record high of 635.88, buoyed by Bayer surging 18.70% on favourable U.S. Supreme Court litigation news.

Asian markets finished mostly down. Japan’s Nikkei 225 closed at 69,360.88 (-2.65%), Hong Kong’s Hang Seng Index at 22,671.86 (-7.44%), and South Korea’s KOSPI at 8,411.21 (-5.81%), though China’s Shanghai Composite Index bucked the trend to finish at 4,027.26 (+1.55%).

A sharp reversal in AI sentiment ignited the global tech rout. Despite Micron Technology surging 15.7% earlier on a blockbuster earnings beat, a steep 6.1% drop in Apple sparked widespread margin compression fears. Apple’s hardware price increases across Macs and iPads highlighted rising pass-through costs of memory chips, dragging tech giants like Microsoft, Nvidia, and Palantir toward deep multi-week or annual lows.

In currency and digital asset markets, the U.S. dollar consolidated its multi-week strength, stabilising the EURUSD pair around 1.135. At the same time, cryptocurrencies faced heavy selling pressure amid the broader de-risking of technology assets.

Meanwhile, the People’s Bank of China (PBoC) left its benchmark Loan Prime Rates unchanged for the 13th consecutive month, maintaining the one-year LPR at 3.00% and the five-year LPR at 3.50%, emphasizing its commitment to policy stability amid an uneven economic recovery. While exports, manufacturing, and industrial production remain relatively resilient, weak consumer spending, subdued business confidence, and the prolonged property sector downturn continue to suppress domestic demand.

The central bank is therefore prioritizing targeted liquidity support and improved credit transmission over further rate cuts, recognizing that weak credit demand, not borrowing costs, is the key constraint. As a result, authorities are expected to lean more on targeted fiscal measures and sector-specific interventions to support consumption, stabilize the property market, and sustain growth while safeguarding financial stability.

The World Economic Forum (WEF) Summer Davos 2026, held on June 22–25, revealed a consequential message: global competitive advantage is shifting from innovation leadership to execution leadership. As artificial intelligence, advanced manufacturing, and sustainability technologies become increasingly accessible, the key differentiator for businesses will be their ability to deploy these capabilities at scale and translate them into measurable productivity gains. The success of the latest Global Lighthouse Network cohort demonstrates that firms integrating AI, workforce transformation, and resource efficiency across entire value chains are achieving superior operational performance, stronger resilience, and enhanced profitability. For investors, this signals that future valuation premiums may increasingly accrue to companies capable of converting technological adoption into sustainable earnings growth, rather than those relying solely on innovation narratives or research intensity.

The global commodities markets remained highly volatile as easing geopolitical tensions and evolving US-Iran peace negotiations drove broad price movements. Brent crude traded within a range of $72.33–$77.70/bbl., while WTI crude fluctuated between $69.07/bbl. and $73.68/bbl., reflecting concerns over increased Iranian oil supply, recovering exports through the Strait of Hormuz, and expectations of a potential global supply surplus. Gold traded between $3,984.36/oz and $4,178.12/oz, initially benefiting from safe-haven demand before retreating sharply as easing Middle East tensions, a stronger US dollar, and expectations of prolonged hawkish US Federal Reserve policy reduced investor appetite for the non-yielding asset.

The near term remains data-driven and cautious as Q2 2026 draws to a close, with upcoming inflation prints, FX trends, and monetary policy signals expected to anchor market direction, including the CBN’s 306th MPC meeting decision in July 2026. Locally, liquidity management and FX stability from the Central Bank of Nigeria, alongside global inflation and labour data shaping US rate expectations, will remain key drivers of volatility and risk sentiment. Sticky inflation or delayed disinflation may sustain the higher-for-longer narrative, keeping FGN bond yields elevated above 18% and reinforcing strong demand for OMO and NTB instruments. A downside inflation surprise or softer policy stance could prompt selective re-entry into mid- and long-dated bonds.

By: Sandra A. Aghaizu

The market walks a narrow lane,

Where calm and storms both leave their stain.

Each whisper of the wind brings change,

As fortunes shift and paths rearrange.

The patient tree grows deep, not fast,

Its strongest roots are built to last.

For those who watch with steady eyes,

Tomorrow’s harvest crowns the wise.