Weekly Market Review

Financial markets ended the week in a bearish repricing phase, driven by tighter liquidity expectations, elevated sovereign supply, and shifting geopolitical and monetary signals. In Nigeria, fixed-income assets weakened sharply as T-bill and bond yields surged on aggressive selloffs and anticipation of heavier DMO issuance, with the planned ₦1.20tn FGN bond auction and steepening NTB curve reinforcing a higher-for-longer rate environment amidst sticky inflation. Equities mirrored the risk-off tone, extending losses on broad-based profit-taking in heavyweight stocks, while FX conditions remained relatively volatile, despite rising reserves above the $50bn mark. Globally, markets were split between geopolitical relief and renewed central bank hawkishness, lifting US and select Asian equities while weighing on Europe and commodities, as oil prices softened on easing supply risks, and gold retreated under higher yield pressure. Overall, the week reflected risk hedging, selective duration appetite, and continued repricing across fixed income, equity, and commodity markets. Commodities closed positive week-on-week (WoW), with Brent crude and West Texas Intermediate (WTI) at $80.59/bbl. (-7.47%) and $77.33/bbl. (-8.40%) respectively, while gold declined at $4,151.74/oz (-1.58%).

Interbank liquidity remained robust through the week within the range of ₦3.40trn, peaking at ₦5.17trn before recording a deficit of ₦3.77trn on Friday (-216.25% WTD). Money market rates were stable, with the Open Repo Rate (OPR) at 22.00% and the Overnight (O/N) rate at 22.20% (+0.4bps). In the FX market, the Naira traded within a range of $/₦1,354.50 and $/₦1,374.00, before closing at $/₦1,370.46 on Friday.

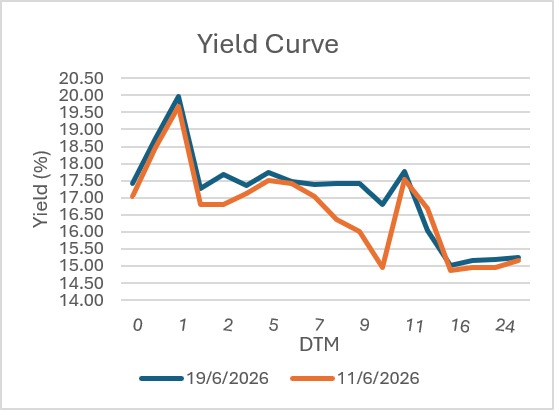

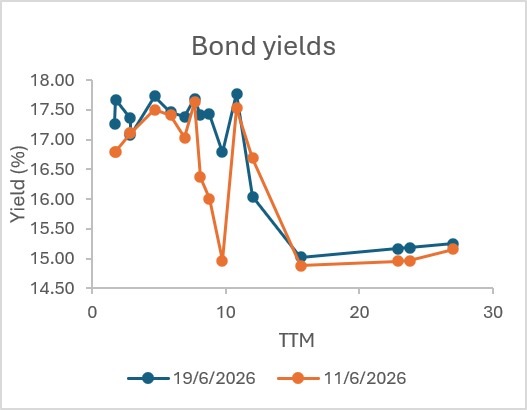

The fixed income market recorded a broadly bearish week as investors repositioned ahead of auctions and adjusted portfolios to reflect expectations of a higher interest rate environment. In the T-bills market, one-year yields rose by ~40bps to 17.74%, driven largely by selloffs across the mid-to-long tenors as participants reduced holdings and sought better entry levels ahead of primary market supply, although selective buying interest remained visible across parts of the curve, particularly the long end. OMO bills maintained the upper-19% yield range. Similarly, the FGN bond market weakened, with offer for mid-tenor yields climbing from 16.95% to 17.80%, reflecting pressure from expectations of increased issuance and improved investor’s appetite, particularly across the short and belly segments of the curve. Trading activity remained concentrated in benchmark sovereign papers, with robust activity on 2029 – 2037, with 2035, 3037 consistently dominating volumes. Overall, the week signalled cautious investor sentiment, preference for yield preservation, and continued repricing of sovereign fixed income assets amid elevated supply expectations and a higher rate environment.

The Debt Management Office (DMO) released its offer circular for its Monday, June 22, 2026, FGN Bond auction, marking +100% increase from the previous auction volume to ₦1.20tn from ₦600.00bn. Marking the highest offer volume in the year, the increase reflects a shift in funding need, with equal offer volume split between the two reopened long tenor papers [22.60% FGN JAN 2035 AND 16.2499% FGN APR 2037]. The revision points to active debt management aimed at optimizing refinancing costs and further soaking up liquidity in the system while catering to fiscal funding needs.

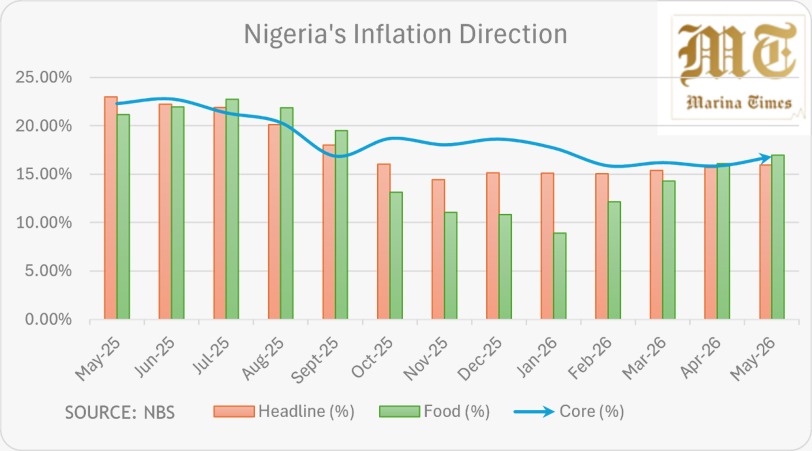

The May 2026 Consumer Price Index (CPI) report published by the Nation’s National Bureau of Statistics (NBS), indicates a modest monthly uptick in the price level, with the index increasing to 140.7 (+2.4points) with monthly inflation indices (marking third uptick in the year); Headline inflation at 15.93% (+24bps), Food inflation at 16.96% (+90bps), and Core at 16.82% (+96bps) signalling short-term price pressures. The broader inflation picture remains supported by significant year-on-year (YoY) declines across key measures: headline, food, and core at -10.13%, -7.59%, and 8.10%, respectively. Highlighting reduced underlying price momentum outside volatile food and energy components. Urban inflation (16.07%) remains marginally higher than rural (15.60%), suggesting stronger price transmission in urban markets, though both are trending lower compared to the prior year. The 12-month average inflation rate also fell substantially to 18.36% from 30.57%, reinforcing a broad-based easing trend. However, food items remain the dominant driver of inflation, with persistent pressures in staples like yams, maize, tomatoes, and cassava, while state-level data shows wide dispersion, indicating uneven inflation dynamics across regions. Overall, the report points to moderating inflationary pressures, but with sticky food and core components still anchoring prices above comfort levels.

The latest T-bill auction held on June 17, 2026 reflected a clear steepening bias, with stop rates rising across all tenors: 91-day at 16.28% (+23bps), 182-day at 16.50% (+31bps), and a sharper repricing in the 364-day to 17.34% (+99bps), driving effective yields higher to 16.97%, 17.98%, and 20.97%, respectively. Market demand showed a pronounced barbell structure, with strong subscription in the short and long ends (91-day and 364-day oversubscribed at 1.29x and 2.08x, with the long end notably stronger on broader demand skew), while the 182-day mid-tenor was relatively weak at 0.70x, highlighting investor preference. Although total demand declined by 13.8% compared to the prior auction, the DMO increased sales by 2.3%, clearing roughly 80% of total bids (NGN1.86tn) at higher stop rates, effectively lifting government funding costs. Overall, the auction signals sustained tightening bias in money market pricing.

AUCTION DATE | 17-06-2026 | 17-06-2026 | 17-06-2026 |

MATURITY DATE | 17-09-2026 | 17-12-2026 | 17-06-2027 |

TENOR | 91-DAY | 182-DAY | 364-DAY |

OFFER (₦) | 100,000,000,000 | 100,000,000,000 | 800,000,000,000 |

SUBSCRIPTION (₦) | 129,690,708,000 | 70,224,526,000 | 1,663,486,372,000 |

ALLOTMENT (₦) | 129,320,707,000 | 70,169,526,000 | 1,291,443,371,000 |

BID RANGE (%) | 15.5000 – 18.0000 | 15.5000 – 17.0000 | 16.0000 – 21.0000 |

STOP RATES (%) | 16.2800 | 16.5000 | 17.3400 |

PREVIOUS STOP RATES (%) | 16.0500 | 16.1900 | 16.3500 |

The Nigeria Revenue Service (NRS) has issued a transition guidelines to support the implementation of Nigeria’s new tax regime and provide clarity for taxpayers, investors, and revenue authorities as the country moves into one of its most significant fiscal reforms in decades. A central feature of the framework is that all tax liabilities, audits, investigations, disputes, and obligations relating to periods before 1 January 2026 will continue to be administered under the repealed tax laws, while obligations due from that date onward will fall under the new tax framework. Importantly, existing tax incentives and exemptions granted under previous legislation will remain valid until their expiry dates, reducing policy uncertainty and preserving investor confidence, although new incentive applications will now be assessed under the Tax Acts 2025. The guidelines also clarify the treatment of income taxes, transaction taxes, development levies, filings, and record-keeping across overlapping tax periods, with implementation anchored on principles of clarity, fairness, and administrative certainty to drive compliance, harmonise tax administration, and strengthen Nigeria’s investment attractiveness without retroactive application of the new laws.

The Naira was volatile during the week in the Nigerian Foreign Exchange Market (NFEM), with a loss of ₦14.19 (+1.05%) week-to-date (WTD), and ₦6.63 (+0.49%) WoW, before closing at $/₦1,370.46 (WoW ₦1,363.83). Foreign reserves advanced its ascent up the $51bn mark to record $51.04bn (+1.21%) as of June 18, 2026, leading to a corresponding decline in blocked funds to $671.72m (-0.09) with an eased blocked reserve ratio of 1.32% (-0.1bps), signifying a relatively stable foreign exchange condition despite external pressures.

The Nigerian equities market recorded a broadly bearish week as sustained selloffs in large-cap stocks dragged performance lower across five consecutive sessions. The NGX ASI declined from 243,271.57 points to 235,941.27 points (WTD -3.01%, WoW -3.59%), reducing the year-to-date return from 57.27% to 51.62%, as investors engaged in profit-taking across major names including ARADEL, GTCO, ZENITHBANK, DANGCEM, FIRSTHOLDCO, and GEREGU. Amid a bullish close of Aradel (+4.8%) on Friday. Market capitalization (eased from ₦157.86trn to ₦153.37trn) and sentiment remained weak despite pockets of increased participation and stronger midweek trading value, with market breadth undulating between 0.13x and 0.45x, consistently negative as decliners outpaced gainers throughout the week. Sector performance was largely subdued, led by losses in Banking, Insurance, Oil & Gas, and Industrial Goods, while Consumer Goods also remained under pressure. Overall, the week reflected cautious investor positioning, reduced risk appetite, and continued rotation away from heavyweight counters despite resilient transaction values and intermittent buying interest in select names.

The Nigerian Exchange’s new three-tier trading framework represents a structural recalibration of price discovery rather than a directional market policy. By replacing the uniform 100,000-unit minimum execution threshold with a graduated model, Group A: 10,000 units for stocks priced at ₦1,000 and above, Group B: 50,000 units for stocks between ₦500–₦999, and Group C: 100,000 units for stocks below ₦500, NGX aligned price sensitivity with stock valuation and market depth. The reform effectively revives elements of the pre-2018 market microstructure regime and is designed to reduce disproportionate price swings caused by low-volume trades, particularly in high-priced equities, while strengthening market integrity and improving pricing efficiency. For institutional investors, the change could enhance confidence in valuation signals and reduce short-term distortions; however, for less liquid names, higher trade thresholds may slow price adjustment and dampen responsiveness to new information. The broader implication is that NGX is moving toward a more mature liquidity architecture amid rising retail participation, deeper market sophistication, and ongoing reforms aimed at improving transparency, execution quality, and capital market competitiveness.

Global financial markets wrapped up a pivotal week on a highly resilient note, driven by major geopolitical relief and a semiconductor-led tech rally that pushed Wall Street indices like the S&P 500 and Nasdaq higher. WoW, equities closed positive: the Nasdaq Composite at 26,517.93 (+3.10%), S&P 500 at 7,500.58 (+1.64%), and the blue-chip Dow Jones Industrial Average at 51,564.70 (+1.28%). Across Europe, Germany’s DAX 40 closed at 24,985.82 (+2.10%), while the FTSE 100 eased at 10,363.27 (-1.15%). Asian markets finished down, with Japan’s Nikkei 225 at 71,250.06 (+3.25%), China’s Shanghai Composite Index at 4,090.48 (+1.81%), Hong Kong’s Hang Seng Index at 23,924.81 (-3.21%), and South Korea’s KOSPI at 9,052.42 (+11.43%). Investor sentiment was sharply boosted by the signing of a landmark interim peace agreement between the United States and Iran, which effectively reopened the Strait of Hormuz and caused crude oil prices to ease significantly below the $80/bbl. threshold. This geopolitical breakthrough helped offset an overwhelmingly hawkish macroeconomic backdrop dominated by top-tier central bank decisions. The Federal Reserve, meeting under new Chair Kevin Warsh, unanimously held its benchmark rate steady at 3.50%–3.75% but delivered a hawkish shift by cutting out easing-leaning forward guidance and flashing a dot plot where most officials projected a potential rate hike before the end of the year. Mirroring this caution, the Bank of England held its base rate at 3.75% in a 7-2 vote, citing a desire to ensure recent underlying disinflation is durable, as UK inflation (CPI) unexpectedly held steady at 2.80% YoY and 0.20% MoM for May 2026, defying fears of an energy-driven spike. On the high-street front, UK retail sales volumes provided a resilient consumer surprise, rebounding sharply by 1.2% month-on-month in May on the back of promotional activity and warmer weather. Meanwhile, the Bank of Japan provided the week’s biggest hawkish surprise, voting 7-1 to raise its policy rate from 0.75% to 1.0%, its highest level since 1995, as a weak Yen hovering near 160 per dollar and persistent wholesale inflation forced policymakers to dial back monetary accommodation despite the temporary medical absence of Governor Kazuo Ueda.

African financial markets closed the week with resilient but uneven performance as easing geopolitical risks, targeted policy support, and development financing shaped investor sentiment across the continent. In South Africa, inflation accelerated to 4.5% year-on-year in May while core inflation remained contained, reinforcing expectations that the central bank may maintain a cautious policy stance amid softer oil prices and improving inflation dynamics. Sentiment was further supported by the BRICS-backed New Development Bank’s approval of up to US$1 billion to upgrade urban infrastructure across major metropolitan areas. In West Africa, Sierra Leone secured a US$211.5 million IMF climate resilience facility alongside a US$31.7 million disbursement under its Extended Credit Facility, strengthening external buffers and climate preparedness. Eastern and Northern African markets remained constructive, with sustained turnover supporting gains in regional equities and Egypt’s benchmark market extending its strong year-to-date performance, highlighting continued investor appetite despite a complex macro backdrop.

The global commodities market closed the week with heightened volatility driven by shifting geopolitical sentiment and central bank repricing. Gold traded within a weekly range of $4,165.05–$4,363.24/oz, initially rallying above $4,300/oz on optimism surrounding the anticipated US–Iran peace agreement and the expected reopening of the Strait of Hormuz, before reversing sharply as hawkish signals from the US Federal Reserve strengthened expectations for further rate tightening and lifted the opportunity cost of holding non-yielding assets. By Friday, gold had fallen below $4,200/oz, erasing earlier gains. In energy markets, crude and Brent experienced broad downside pressure despite a late-week rebound, with WTI crude trading within $75.15–$80.23/bbl. and Brent within $78.08–$82.75/bbl., during the week. Prices declined as easing Middle East supply concerns, improving shipping activity through Hormuz, and expectations of recovering production outweighed intermittent geopolitical setbacks, positioning oil for one of its sharpest weekly pullbacks in recent months.

The new week is set for defining events from the June 2026 FGN Bond auction of 1.2trn in offer, continued preference for long-day bills as the CBN sustains liquidity management through OMO operations, keeping bond yields volatile, and T-bill demand on defensive positioning. Equities are likely to mirror cautious positioning while FX stability persists, supported by improved reserves and steady inflows. Anticipated liquidity inflows of over ₦3.45trn, comprising FGN Bond coupon totalling ₦423.51bn from 2032s, 2033s, 2038s, and 2053s, ₦97.75bn, and ₦2.63trn in maturing NTB and OMO maturities, respectively, all of which are anticipated to influence investors’ positioning.

By: Sandra A. Aghaizu

Gold climbed the hill on whispers of peace,

A shining kite beneath calmer skies.

But the wind of rates blew cold and fierce,

And pulled its golden wings from the rise.

Oil was a river swollen with fear,

Flowing fast through narrow straits.

Yet when the storm clouds drifted clear,

The waters fell beneath their weight.

So markets danced like leaves at sea,

Between hope’s light and caution’s call.

For every rise that greets the dawn,

A shadow waits beyond it all.

Subscribe now to keep reading and get access to the full archive.