July 2026, Edition 2

Nigeria’s financial markets entered a phase of renewed optimism during the week ended July 10, 2026, as fixed income yields eased due to improving foreign exchange (FX) fundamentals and investor sentiment across asset classes, including equity. Strong demand for government securities compressed yields across the curve, while the Nigeria Treasury Bill (NTB) auction revealed a market concerned about duration despite higher return expectations. The Naira’s stability, record-high external reserves, and declining blocked funds emphasized confidence in the FX market, even as global inflation risks and geopolitical tensions kept investors cautious. Equities extended their rebound on renewed institutional accumulation, while global markets navigated a delicate balance between resilient growth, elevated commodity risks, and tighter financial conditions. Overall, the week highlighted a market environment where liquidity, positioning, and policy expectations remain the dominant forces shaping asset allocation decisions. Commodities closed week-on-week (WoW) higher, with Brent crude and West Texas Intermediate (WTI) at $76.01/bbl. (+5.47%) and $71.41/bbl. (+3.91%) respectively, while gold at $4,121.05/oz (+0.79%).

Interbank liquidity remained robust through the week, opening at ₦2.31 trillion, peaking at ₦4.87 trillion before closing at ₦ 4.33 trillion on Friday (-3.30% WTD). Money market rates were stable, with the Open Repo Rate (OPR) at 22.00% and the Overnight (O/N) rate at 22.23% (WoW +5bps). In the FX market, the Naira traded within a range of $/₦1,366.00 and $/₦1,387.00, before closing at $/₦1,379.62 on Friday.

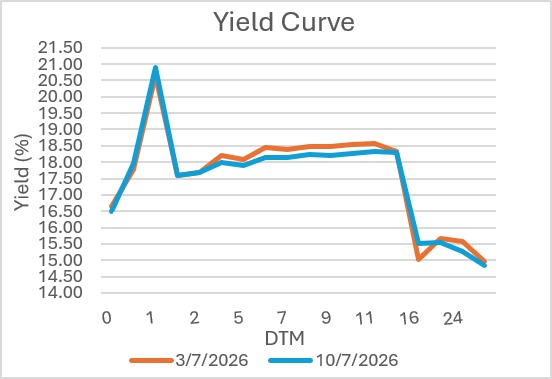

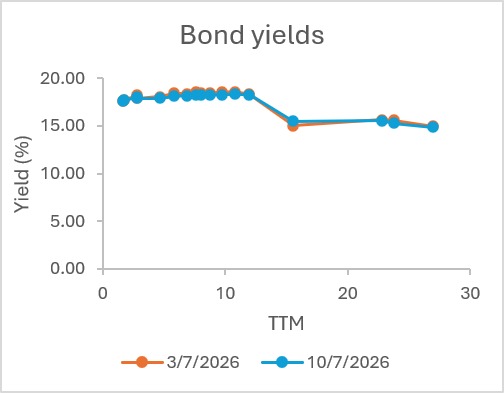

The fixed income market maintained a bullish tone during the review period, as sustained demand across Treasury Bills (T-Bills), Open Market Operations (OMO) instruments, and FGN Bonds drove a gradual compression in yields. T-Bills traded within the 17.00%–17.50% range, with increased buying interest on the short-to-mid tenor maturities in addition to the newly issued Jul-2027 bill, while OMO bills continued to attract demand at elevated rates around the 19.65%–21.10% level, reflecting selective preference for attractive returns. In the FGN bond space, buying interest was concentrated around short-mid tenor benchmark maturities (2029-2038s), with rates generally easing toward the 18.00%–18.30% levels by Friday, with renewed mild interest for longer tenors including 2049s, 2050s, and 2053s (indicating long-term yield locking and avoidance of reinvestment risk). Overall, the week’s activity points to renewed investor appetite for duration assets amid expectations of further yield moderation, although elevated short-term rates suggest liquidity, sentiment, and positioning ahead of upcoming primary market activities, and monetary policy signals remain a key market driver.

Primary Issuance Brief: The July 08, 2026, NTB primary market auction heavily highlighted a skewed preference for short- and long-day risk-free assets, fuelled by a cash surge from recent OMO maturities that boosted system liquidity. While demand at the short end was mixed, the 91-day bill oversubscribed at 1.47x, and the 182-day bill undersubscribed at 0.30x, the 364-day long-tenor paper saw overwhelming interest with about 3.71x oversubscription. To sterilize the system’s excess liquidity, the Central Bank of Nigeria (CBN) allotted 87% in excess of the initial offer on the 364-day paper, pushing its stop rate up by 36 basis points, while the 91-day inched up by 2bps and the 182-day remained unchanged. Effective yield was 16.99% (+2bps), 17.98%, and 21.97% (+52bps) for the short-, mid-, and long-day, respectively. This upward repricing signals that despite robust system liquidity, institutional investors are successfully demanding higher premium compensation to lock up funds. Total demand improved by 9.09% compared to the last auction. However, the Debt Management Office’s total sales declined by 28.60%, with allotment of NGN1.06trn (52.36%) of the total demand. Indicating cost management despite robust demand at the cleared stop rate.

AUCTION DATE | 08-06-2026 | 08-06-2026 | 08-06-2026 |

MATURITY DATE | 08-10-2026 | 07-01-2027 | 08-07-2027 |

TENOR | 91-DAY | 182-DAY | 364-DAY |

OFFER (₦) | 100,000,000,000 | 100,000,000,000 | 500,000,000,000 |

SUBSCRIPTION (₦) | 146,544,502,000 | 29,936,835,000 | 1,856,310,301,000 |

ALLOTMENT (₦) | 115,383,380,000 | 13,760,461,000 | 935,316,907,000 |

BID RANGE (%) | 15.5000 – 18.0000 | 15.7500 – 17.3000 | 16.5500 – 20.3200 |

STOP RATES (%) | 16.3000 | 16.5000 | 17.7000 |

PREVIOUS STOP RATES (%) | 16.2800 | 16.5000 | 17.3400 |

The Naira gained during the week in the Nigerian Foreign Exchange Market (NFEM), gaining ₦11.35 (+0.83%) week-to-date (WTD), and ₦9.43 (+0.69%) WoW, before closing at $/₦1,379.62 (WoW: ₦1,370.19). Foreign reserves increased to a record $51.74bn (+0.55%) as of July 09, 2026, resulting to a decline in blocked funds to $633.23mn (-2.40%) with a reduced blocked reserve ratio of 1.23% (-0.4bps), marking an improved foreign exchange condition despite external pressures.

The International Monetary Fund (IMF) recent revised global economic growth forecast suggests the global economy has avoided the worst-case fallout from the Middle East conflict, but the price of that resilience is a weaker and more inflation-prone near-term outlook. Global growth for 2026 was trimmed from 3.1% (April 2026 projection) to 3.0% and 3.4% for 2027, while global inflation was raised to 4.7% from 4.1%, reflecting the pressure of energy prices that are now 25% above pre-war levels. Contrastingly, Sub-Saharan Africa (SSA) was amended from 4.5% to 4.3% in 2026 and 4.5% in 2027, while Nigeria’s economy is projected to expand by 4.1% in 2026 and 4.3% in 2027. In effect, the IMF is signalling that the world is still growing, but under tighter conditions where geopolitical risk, costlier oil and trade fragmentation are beginning to weigh more visibly on momentum. The divergence in country forecasts underlines the uneven global outlook: energy-exporting and technology-linked economies such as China showed greater resilience, while commodity-importing countries and regions more exposed to conflict have faced steeper downward revisions as higher energy costs and geopolitical disruptions weigh more heavily on growth prospects. The rebound projected for 2027 offers some reassurance, but the broader message is that the global economy is entering the second half of 2026 with less growth, more inflation pressure and a much thinner margin for new shocks.

The Nigerian equities market recovered from the previous week’s drawdown during the week, with the Nigerian Exchange (NGX) ASI advancing for four consecutive sessions before closing lower on Friday at 243,954.45 points, marking a 4.17% WTD and 6.42% WoW, lifting year-to-date returns from 47.31% to 56.77%. The bullish momentum was largely driven by renewed investor repositioning and strong accumulation in large-cap counters, including AIRTELAFRI, DANGCEM, WAPCO, ARADEL, and FIRSTHOLDCO, following the recent market correction, performance reports, and prospective reclassification on global indices. Market capitalisation expanded to ₦158.58trn from ₦152.23trn, reflecting broad-based gains across key sectors, with Industrial Goods, Banking, Oil & Gas, Consumer Goods, and Insurance indices contributing to the recovery. Investor activity strengthened significantly, culminating in a surge in turnover on Thursday as FIRSTHOLDCO’s block trades lifted total market value traded to ₦111.96bn, although market breadth moderated toward the weekend (4.36x to 2.17x), suggesting selective profit-taking and demand. Overall, the market’s strong rebound signals improved risk appetite and renewed confidence in fundamentally strong equities. Other developments during the week include:

Global financial markets showcased remarkable resilience as late-week AI-driven tech momentum successfully countered earlier macroeconomic anxieties and geopolitical flare-ups. Investors navigated mixed data from the United States, where the economic landscape remained on steady footing as the S&P Global Composite PMI improved to 52.2 and the ISM Services PMI registered a sturdy 54.0, reinforcing services-led expansion despite a widening May balance of trade deficit, which surged to $77.6 billion. Across the Atlantic, deeper property-market strains weighed heavily on European sentiment as June S&P Global Construction PMIs painted a stark picture of contraction, falling further to 42.8 in the Eurozone and hovering near critical lows at 38.4 in the United Kingdom. This regional stress was vividly reflected in the fixed-income space, where fiscal and inflationary anxieties pushed France’s 30-year government bond yield to an all-time high of nearly 4.71% and dragged the UK 10-year gilt yield to a multi-week peak of 4.95%. Meanwhile, U.S. sovereign debt experienced a highly volatile week; the benchmark 10-year Treasury yield surged to a seven-week high of nearly 4.60% amid escalating U.S.-Iran tensions before retracing back down to 4.54% following solid auction demand. In Asia, China’s foreign exchange reserves pulled back by 0.75% to $3.416 trillion due to a stronger U.S. dollar and valuation shifts, yet the underlying tech-heavy equity rally managed to carry major global indices into winning territory by the week’s close. The equities market performance varied, closing WoW at: the Nasdaq Composite at 26,281.61 (+1.70%), S&P 500 at 7,575.39 (+1.20%), and the blue-chip Dow Jones Industrial Average at 52,637.01 (-0.50%). Across Europe, Germany’s DAX 40 closed at 25,067.09 (-2.90%), while the FTSE 100 was at 10,497.29 (-1.70%), and the Stoxx 600 at 641.10 (-1.79%). Asian markets were mixed, with Japan’s Nikkei 225 at 68,557.73 (+0.49%), China’s Shanghai Composite Index at 3,996.16 (-1.17%), Hong Kong’s Hang Seng Index at 24,175.12 (+3.53%), and South Korea’s KOSPI at 7,475.94 (-7.60%).

West Africa Economic Overview: Ghana is strengthening its fiscal credibility and external debt sustainability under its Eurobond Debt Exchange Programme, having repaid $2.1bn to Eurobond holders since January 2025, which includes an early $700mn settlement on July 2, 2026 ($525.2 million principal, $174.8 million interest) that prevented pressure on foreign reserves. Concurrently, as neighbours like Nigeria eye a return to the Eurobond market, Ghana is combating a 50,000-tonne unsold bean surplus and weaker global demand by diversifying into high-value, semi-processed cocoa exports (liquor, butter, cake, powder) through new supply commitments with the UAE and Saudi Arabia. This sovereign positioning is further boosted by the ECOWAS Bank for Investment and Development (EBID) approving over $417 million in regional project financing, including $260 million for Nigeria’s Trans-Saharan Highway and $47.4 million for Ghana’s Black Volta Gold Project, alongside a strategic plan to double its balance sheet to $4.4 billion over five years to help bridge West Africa’s $36 billion infrastructure gap.

The World Bank Group’s 2026–2027 income classification update saw six economies move into higher income categories, reflecting different growth trajectories, from export-led expansion to economic recovery and improved statistical measurement. Vietnam, the Philippines, Sri Lanka, Jordan and Micronesia advanced from lower-middle to upper-middle income, while Togo moved from low to lower-middle income. Vietnam’s upgrade was driven by strong export performance and sustained growth, with GDP expanding 7% in 2024 and 8% in 2025; the Philippines benefited from broad-based economic expansion averaging 5.8% annual GDP growth over five years; Sri Lanka’s reclassification reflected a post-crisis rebound with 5% GDP growth in 2025; Jordan crossed the threshold after a national accounts revision showed its economy was nearly 10% larger than previously estimated; Micronesia gained from steady recovery-led growth, while Togo’s upgrade was largely influenced by an 11.7% downward population revision, which lifted per capita income metrics alongside 5.9% GDP growth in 2025. No country was downgraded in the latest review, highlighting continued long-term global income mobility despite uneven development paths.

Global commodities markets swung sharply this week as supply-side fundamentals repeatedly collided with geopolitical risk in the Middle East. Brent and WTI opened weaker on expectations of higher OPEC+ output, recovering tanker traffic through the Strait of Hormuz and Saudi price cuts to Asia, but rebounded strongly midweek after renewed attacks on vessels in Hormuz, fresh US strikes on Iran and retaliatory Iranian action reignited fears of supply disruptions through the critical shipping corridor. Brent climbed from around $71.90/bbl. at the start of the week to as high as $78.50/bbl. midweek before easing to $76.00/bbl. by Friday, while WTI moved from $68.60/bbl. to a peak of $73.90/bbl. before settling near $71.40/bbl. In contrast, gold traded in a volatile but largely range-bound pattern, pressured early in the week by a firmer dollar and expectations of tighter US monetary policy, before drawing intermittent safe-haven support from the same Middle East tensions. Bullion briefly fell from $4,143.43/oz toward $4,030/oz on Wednesday before recovering to close the week around $4,121/oz, leaving it broadly flat as investors balanced geopolitical uncertainty against persistent concerns that higher oil prices could keep inflation elevated and reinforce the Fed’s higher-for-longer stance.

OPEC+ approved a further 188,000 bpd output increase for August 2026, extending its supply restoration even as actual production remains below pre-war levels due to disruptions in the Strait of Hormuz. While the seven core producers have raised quotas in the year by nearly 800,000 bpd since April, OPEC output still fell to 33.13 million bpd in May from 42.77 million bpd in February before showing signs of recovery in June. With Brent back near $72/bbl. from highs above $120/bbl., the market is increasingly focused on recovering Hormuz exports, weaker Chinese demand and rising non-Middle East supply, while OPEC+ now has about 379,000 bpd left to restore if it completes one final hike in September 2026.

Nigeria’s UTM Offshore has cleared a major hurdle for its $3 billion floating LNG (FLNG) project after securing a 15-year gas supply agreement with a joint venture between NNPC Ltd and Seplat Energy Producing Nigeria Unlimited. The deal will provide 200 million standard cubic feet of gas per day from the Yoho field, supporting the project’s planned 1.8 million tonnes per year LNG production capacity and paving the way for a final investment decision expected in Q4 2026. The FLNG project, in which UTM Offshore holds 72%, NNPC 20% and Delta State Government 8%, represents a key step in Nigeria’s drive to monetise its vast gas reserves, expand LNG exports and address longstanding challenges around stranded gas development, infrastructure and investment funding.

Markets are expected to remain optimistic, carefully supported by improving liquidity conditions and investor appetite, while yield movements, FX stability, and global risk factors remain key drivers of near-term direction. Expected inflows in the week are over ₦3.04trn (₦2.97trn in OMO maturity, ₦65.36bn for FGN 12.15% Jul. 2034), with a scheduled NTB auction of ₦600.00 billion and offer ratio split across the 91-, 182-, and 364-day bills in 1:1:4. The June 2026 Inflation data, expected during the week, is a key market direction driver, as a third consecutive MoM increase despite YoY moderation could shape expectations and policy direction ahead of the upcoming Monetary Policy Committee meeting.

By: Sandra A. Aghaizu

Money flows like a river after the rains,

Filling dry streams with renewed hope.

Yet every traveller pauses at the crossroads,

Waiting for the wind to reveal its direction.

Inflation whispers through the trees,

While interest rates stand like silent mountains.

The wise investor does not chase every current,

But watches the sky before setting sail.

For every market carries two companions,

Promise in one hand, caution in the other

Subscribe now to keep reading and get access to the full archive.