In a week where headlines depicted volatility, the real story was quieter, and far more telling; Nigeria’s financial market witnessed a calm return to business with liquidity in control after the Easter break.

Despite oil shocks, fragile ceasefires, and global uncertainty, investors leaned decisively into duration and selective risk, compressing front-end Eurobond yields by 28bps, sustaining FGN bond yields in the 16% band, and aggressively absorbing long-dated NTBs and OMO bills at upper-15% and 19% level. Even as the Naira strengthened and equities edged higher, the message across markets was consistent, thereby illustrating a cycle that is no longer a panic-driven cycle, but one cautious repositioning, and capital is not fleeing risk, but repricing it with precision. Week-on-week, oil closed lower with Brent crude and West Texas Intermediate (WTI) at $97.72/bbl. (-10.0%), and $99.57/bbl. (-9.7%), while gold at $4,751.68/oz (+2.8%).

Interbank liquidity opened on Tuesday at a ₦6.17trn surplus, peaking at ₦7.09trn on Wednesday, easing to a close at ₦4.79trn on Friday, marking a week-to-date decrease of 11.4%. Money market rates were relatively stable, with the Open Repo Rate (OPR) steady at 22.00%, while the Overnight rate (O/N) opened at 22.25%, closing at a peak of 22.35%. In the currency market, Naira traded between $/₦1,351.50 and $/₦1,390.00, before winding up at $/₦1,359.00 on Friday.

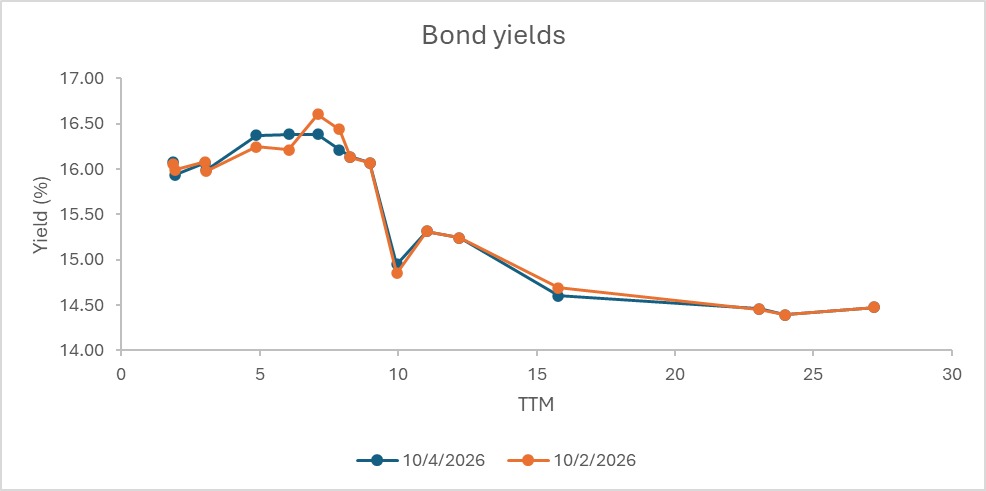

The secondary market largely reflected a mixed bearish-bullish trend, amidst global energy volatility and fragile Middle East peace talks. Though a reactive sentiment and selective preference drove trades, demand focused on the short- and mid-end of the curve, bond yields held around the low-16% level, while long-day Treasury bills hovered within the high-15% to low-16% range, despite lower marginal rates at recent NTB auction. Overall, the market had priced in yield compression, resulting in minimal effect on FGN bonds across 2027–2036 maturities. OMO bills continued to trade firmly near the upper-19% band.

Between March 31 and April 7, 2026, Nigeria’s Eurobond curve reflected a bullish flattening bias, with clear differentiation across tenors. The short end (2027–2028) led the rally, compressing by ~11–28bps, signalling renewed confidence in near-term liquidity and macro stability. The mid-curve (2029–2034) showed mixed but modest movements: 2029 compressed by ~9bps, 2030 widened by ~43bps (the key outlier), while the 2031–2034 segment remained broadly stable with slight compression of ~1–7bps, reflecting ongoing portfolio rotation and macro sensitivity. At the long end (2036–2051), yields compressed gradually by ~10–15bps, pointing to steady real money demand and a cautiously constructive long-term credit view. Overall, the curve dynamics indicate a repricing of Nigeria’s sovereign risk, with strong front-end buying, a stabilising belly, and selective duration extension by institutional investors.

The results of the first NTB auction in Q2 2026, held on April 7, 2026, signalled sustained investor appetite for long-duration bills amidst high system liquidity. The sale had a descending Bid-to-Cover Ratio (BCR) strength across the board at 4.79x, 2.62x, and 1.02x for the 1-year, mid-, and short-day bills, respectively. Despite robust subscriptions, total allotment remained selective at 24.7%, with the 364-day bill as the bulk, allowing the mild compression of yields on the mid- and long-day bill at 16.1900% (-23bps) and 16.1990% (-23.1bps). Notably, the bid range showed a resistance level of 15% level, likely a near-term floor for rates.

AUCTION DATE | 07-04-2026 | 07-04-2026 | 07-04-2026 |

MATURITY DATE | 9-07-2026 | 08-10-2026 | 08-04-2027 |

TENOR | 91-DAY | 182-DAY | 364-DAY |

OFFER (₦) | 100,000,000,000 | 100,000,000,000 | 500,000,000,000 |

SUBSCRIPTION (₦) | 96,777,798,000 | 227,940,312,000 | 2,632,745,513,000 |

ALLOTMENT (₦) | 94,823,297,000 | 87,049,795,000 | 549,504,410,000 |

BID RANGE (%) | 15.0000 – 18.0000 | 15.0000 – 17.0000 | 15.0000 – 20.0000 |

STOP RATES (%) | 15.9500 | 16.1900 | 16.1990 |

PREVIOUS STOP RATES (%) | 15.9500 | 16.4200 | 16.4300 |

The April 9, 2026, OMO auction showed the Central Bank’s intensified liquidity sterilisation stance, alongside a clear bias toward locking in short-to-mid duration funds. Total subscriptions surged to ₦2.54 trillion against a ₦600 billion offer, translating to an aggregate bid-to-cover ratio of 1.10x, strongly driven by demand for the 138-day bill at 87.8% (7.45x offer cover), with full allotment executed at a stop rate of 19.91%, highlighting the CBN’s readiness to absorb excess liquidity at elevated cost in pursuit of price stability. Conversely, the 75-day bill saw a more measured approach despite modest demand (1.03x offer cover), only 0.25x was allotted (25.8% of the offer) at a marginal rate of 19.89%, indicating a selective stance at the short end. Overall, the split allocation pattern signals a deliberate strategy to anchor higher duration while maintaining pricing discipline on near-term maturities.

AUCTION DATE | TENOR | OFFER (₦‘B) | BIDS (₦‘B) | TOTAL SALE (₦‘B) | STOP RATES (%) | PREVIOUS TENOR STOP RATES (%) |

09-04-2026 | 75-DAY | 300.00 | 309.50 | 77.50 | 19.8900 | 0.0000 |

138-DAY | 300.00 | 2,236.00 | 2,236.00 | 19.9100 | 19.9100 |

The Naira gained ₦27.99 (-2.15%) week to date, trading within the band of $/₦1,386.66 and $/₦1,356.89 in the Nigerian Foreign Exchange Market (NFEM), and ₦23.90 (-1.73%) week-on-week, closing at ₦1,356.89 (from ₦1,380.79 the previous week). Intra-week movements reflected a resilient market despite relative FX pressures and declining external reserves.

Nigeria’s foreign reserves eased from April 1 to 9, 2026, declining from $49.18 billion to $48.85 billion, with gross reserves of approximately $333.89 million (-0.68%). Blocked funds mirrored the decline from $743.14 million to $738.21 million (-0.66%), and a steady 1.51% blocked reserve ratio, displaying increased external shocks and FX liquidity pressure.

Nigeria’s VAT revenue for Q4 2025 declined by 3.78% QoQ to ₦2.19 trillion, pointing to a modest slowdown in consumption momentum, even as year-on-year growth remained solid at 12.84%. The quarterly dip suggests softening purchasing power toward year-end, as households and businesses adjusted to sticky inflation and energy costs. However, the sustained double-digit annual growth supports structural gains in tax administration and formal sector expansion. Largely reflecting a dual dynamic; a resilient and broadening tax base set against near-term pressure on discretionary spending within a tighter macroeconomic environment. Amid the World Bank cutting Nigeria’s growth forecast to 4.1% (2026) and 4.2% (2027) from 4.4% due to global uncertainty, oil-driven inflation, and weak investment, though stable FX, easing rates, and expansionary index readings indicate resilient near-term growth.

The union of the March 2026 banking recapitalization deadline, Nigeria’s reclassification to FTSE Russell Frontier Market status, and the strategic push for intra-African cross-border listings signalled a fundamental shift from quantitative recovery to qualitative institutional resilience. While the banking sector has successfully crossed the initial capital hurdles, the integration of the CBN’s new Risk-Based Capital (RBC) directive transforms “adequate capital” into a dynamic measure of stress-tested durability, effectively weeding out governance blind spots and insider-exposure risks. This internal systemic strengthening serves as a critical requirement for the global reintegration of the broader capital market; the FTSE upgrade validates improvements in market infrastructure (settlement and transparency), which, when paired with high-impact initiatives like the Dangote Refinery cross-border listing, positions Nigeria as the primary gateway for mobilizing global and continental liquidity. Ultimately, these three pillars, resilient bank balance sheets, international index validation, and regional market integration, collectively transition the Nigerian financial ecosystem from a period of stabilization to one of active capital formation, essential for the nation’s $1 trillion economic ambition.

Amid a period of Banking sector earnings releases, the NGX All-Share Index (ASI) maintained a mild bullish run, opening at 202,023.10 on Tuesday, inching up to 202,584.88 on Wednesday, then further to 203,161.81 by Thursday, and closing at 203,791.18 on Friday. Market breadth activity showed mixed momentum, with volume turnover at 0.71x, 0.58x, 0.92x, and 0.56x indicating cautious investor participation and selective positioning. Top gainers include Zenith, GTCo, WAPCO, Seplat, and Cadbury, while Oando and DANGSUGAR were not so fortunate. Overall, the ASI posted a gain of 0.88% week-to-date (1,768.08 points) and +1.04% week-on-week (2,092.29 points), with the year-to-date at +30.96%.

In the week ended April 10, 2026, global markets sustained a resilient risk-on tone despite persistent macroeconomic pressures. U.S. equities remained firm, with the S&P 500 at ~6,817 and the Nasdaq Composite at ~22,903, while European indices tracked similarly, as the FTSE 100 held near 10,600 and the DAX 40 hovered around 23,768. In Asia, performance was mixed but stable: the Nikkei 225 recovered from earlier volatility at 56,924, the ASX 200 reached ~8,961, and the Hang Seng index traded cautiously around 25,893, reflecting China’s ongoing structural transition with its inflation eased to 1.0% year-on-year (YoY) in March 2026 from 1.3% due to softer food and core demand, following the Lunar New Year, though rising fuel costs and producer prices driven by Middle East tensions signaled a near-term inflation rebound. The macro backdrop remains anchored in a “higher-for-longer” policy regime, with the U.S. Federal Reserve maintaining rates at 3.50%–3.75%, even as March 2026 YoY headline inflation rose to 3.3% (vs. 2.4% prior). Oil markets remained volatile, briefly dipping below $100/bbl., driven by fragile ceasefire dynamics in the Middle East. In response, governments continue to deploy targeted fiscal buffers to mitigate energy cost pressures. Meanwhile, the U.S. 10-year Treasury yield remains a critical valuation anchor across asset classes, with gold, emphasising sustained demand for hedging instruments. In general, markets are navigating a narrow path, balancing growth resilience against inflation persistence, within an increasingly geopolitically sensitive environment.

During the period, commodity markets were dominated by acute volatility across energy and safe-haven assets, driven by shifting geopolitical signals and fragile diplomatic developments. Crude oil prices traded in wide ranges, with WTI declining to ~$109.40/bbl. earlier in the week on ceasefire optimism, surging above $116.00/bbl. on April 7 amid escalation, before sharply correcting by ~15% to $94.91/bbl. following reports of a two-week truce, and ultimately settling higher on Friday at ~$99.57/bbl. Brent mirrored this trajectory, opening at $107.19/bbl. on Monday, peaking above $110.00/bbl., bottoming at $94.72/bbl., and closing at ~$97.72/bbl. on Friday, as intermittent tensions, including disruptions around the Strait of Hormuz, that continued to test the durability of the ceasefire. In parallel, gold exhibited heightened two-way volatility, reflecting a tug-of-war between geopolitical risk and evolving inflation expectations, opening at $4,698.72/oz. on Monday, declining to ~$4,650/oz on Tuesday, midweek at $4,760.83/oz before rallying to a high of $4,791.03/oz on Thursday, and easing to ~$4,751.68/oz by week’s end. Broadly, markets operated in a “controlled risk” environment, where geopolitical shocks are no longer disorderly, but remain materially influential.

In the near term, the market is expected to stay cautiously range-bound, with FGN bond yields at 15.50%-16.10%, while OMOs in the 19% band, and Eurobonds maintain a mild-bullish bias with front-end strength and gradual long-end easing. Supported by expected liquidity of over ₦1.48trn in inflows (₦92.14bn from FGN 19.30% Apr. 2029 coupon payment, and ₦1.39trn from OMOs), though rising anticipation of inflation projected at 16.22% in March 2026, halting an 11-month decline. Driven by a 40% surge in local petrol prices to ₦1,168/L, and increased food costs, posing a risk to the CBN’s 12.94% annual target.

By: Sandra A. Aghaizu

The market did not shout.

It inhaled slowly after the holiday silence.

Liquidity moved like a steady tide,

banks resting on cushions of cash,

while investors stretched their gaze toward the horizon,

placing trust in time rather than urgency.

Oil slipped, gold held its quiet vigil,

and the Naira stood with renewed balance.

Nothing rushed for the exit.

Capital simply adjusted its footing,

not in fear,

but in careful recognition of value

Subscribe now to keep reading and get access to the full archive.