The Nigerian financial markets traded through a week defined by resilient liquidity despite inflation-led repricing pressures and cautious risk-taking across asset classes. Interbank liquidity remained structurally strong, easing from a ₦4.79trn surplus to ₦3.84trn (-22.7% WTD), while money market rates stayed anchored with OPR steady at 22.00% and O/N oscillating around 22.16%–22.35%, reflecting sustained CBN liquidity sterilisation. The FX market maintained relative stability around ₦1,340, supported by mild reserve softening to $48.65bn and a stable blocked funds ratio. However, the fixed income space reacted to March inflation data with a modest upward shift in yields across T-bills, OMO, and FGN bonds, indicating cautious post-CPI repricing rather than broad sell-offs. Equities extended their bullish momentum with the NGX ASI up +6.20% WTD. Eurobonds and global risk assets benefited from easing geopolitical tensions, reinforcing a broadly risk-on but selectively defensive positioned environment. Week-on-week, oil closed on the back of reverse norm with Brent crude at a premium to West Texas Intermediate (WTI) at $90.38/bbl. (-19.1%), and $83.85/bbl. (-17.5%), while gold traded at $4,833.80/oz (+0.8%).

Interbank liquidity opened on Monday at a ₦4.79trn surplus, declining mildly to the ₦3.0trn base during the week, and closed at ₦3.84trn on Friday, a WTD ease of 22.7%. Money market rates were relatively stable, with the Open Repo Rate (OPR) steady at 22.00%, while the Overnight rate (O/N) opened at 22.19%, peaking at 22.35% before closing at 22.16. In the currency market, Naira traded between $/₦1,334.00 and $/₦1,363.00, before winding up at $/₦1,343.64 on Friday.

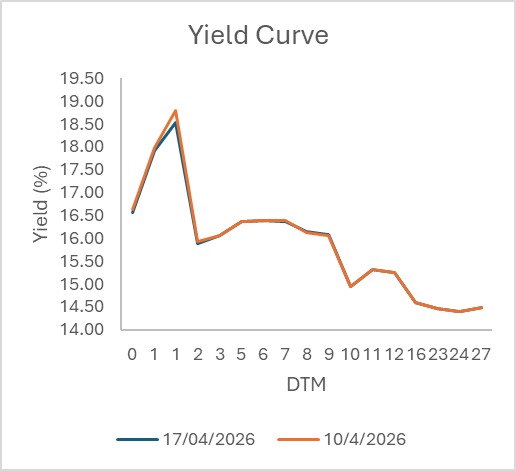

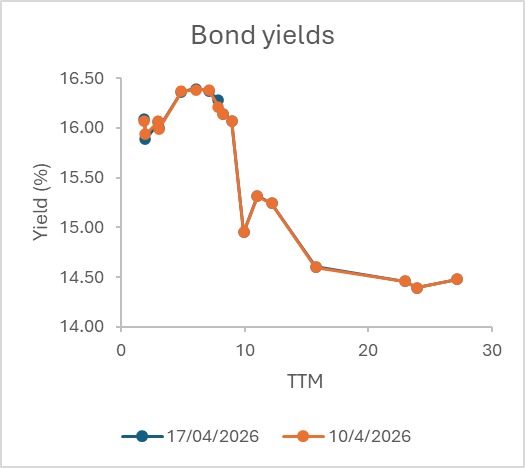

The secondary market traded largely range-bound with a mild bearish momentum, as post-inflation data triggered a slight uptick in yield across the curve. Treasury bills edged higher within 15.70%-16.45%, OMOs stayed sticky around upper-19% levels, while FGN bonds saw average yield inch up by 10-15bps to mid-16% range (with selective preference for the short- and mid-end of the curve). This cautious repricing, rather than broad sell-offs, reflected defensive positioning, but no aggressive market reset.

Nigeria’s Eurobond curve closed (Apr. 8 – 15, 2026) with a bullish bias marked by measurable average yield compression across segments. The short-end (2027–2029) recorded the sharpest decline, tightening by 22bps, reflecting strong front-end demand and liquidity-driven positioning. The mid-curve (2030–2036) followed with a more moderate 23bps, indicating continued risk-on sentiment with selective duration extension. Conversely, the long-end (2038–2051) eased by ~16bps, lagging the rally but benefiting from the improved global risk tone. Overall, the bull curve flattened, with front-end outperforming the bulk of the move while long-duration bonds saw more measured declines.

The April 14, 2026 OMO auction highlights an exceedingly liquid but selectively deployed market, with demand at ₦2.58trn and sales of ₦2.17trn (1.19x offer), strong but moderate from prior levels; demand concentrated on the 7-day (1.87x Bid-to-cover) and 140-day (fully allotted at 1.00x BTC), both clearing at the upper range with stable stop rates (21.90% and 19.91%, respectively), while the 63-day softened, clearing lower at 19.88%, reflecting weak mid-day conviction; effective yields show mild ease at the short-to-mid-day and stability at the long end (7-day: 21.99% ↓2bps vs prior, 63-day: 20.59% ↓7bps, 140-day: 21.56% ↑3bps), reinforcing a steady curve. Overall, the CBN remains firm with liquidity mop-up mode while anchoring rates, amid a market primarily driven by prudent duration positioning rather than directional bets.

AUCTION DATE | TENOR | OFFER (₦‘B) | BIDS (₦‘B) | TOTAL SALE (₦‘B) | STOP RATES (%) | PREVIOUS TENOR STOP RATES (%) |

| 7-DAY | 200.00 | 857.00 | 457.00 | 21.9000 | 21.9000 |

68-DAY | 200.00 | 13.00 | 3.00 | 19.8800 | 19.8900 | |

140-DAY | 200.00 | 1,711.00 | 1,711.00 | 19.9100 | 19.9100 |

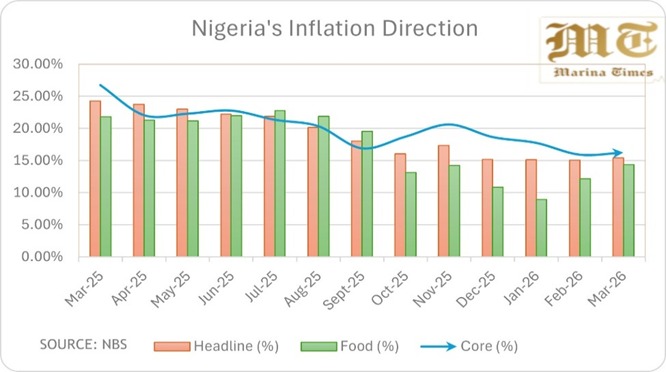

Following the National Bureau of Statistics (NBS) release of Nigeria’s March 2026 CPI data, it becomes clearer when the trends are separated: prices rose sharply in March compared to February, even though the yearly increase looks modest. The consumer price index (CPI) climbed by 5.4 points to 135.4 points, with headline inflation at 15.38% YoY (+32bps), which appears stable at first glance. However, the real signal is in the month-on-month surge of +4.18% (+217bps), showing that prices accelerated significantly in March. This pattern is reinforced by core inflation at 16.21% YoY, which jumped +4.03% MoM (+314bps), indicating broad-based price pressures beyond food, while food inflation at 14.31% YoY (+219bps) masks the broader inflation pickup. The gap between urban (3.16% MoM) and rural (6.73% MoM) inflation also points to stronger price pressures in rural areas. Overall, this report indicates that earlier FX and energy shocks are still feeding through.

OPEC data shows that Nigeria’s crude oil production rose to 1.38 million barrels per day in March 2026, up from about 1.31 mbpd in February, marking a modest recovery but still below its 1.5 mbpd OPEC quota and 1.84 mbpd budget benchmark. The increase was driven by improved output from upstream operations, yet structural challenges and supply disruptions continue to limit full capacity. Notwithstanding the gain, Nigeria retained its position as Africa’s largest oil producer, though it remains under pressure to sustain higher and more stable production levels.

Nigeria’s financial market is undergoing structural strengthening, with key reforms taking effect from May 1, 2026. The CBN’s updated BVN framework, now restricting enrollment to individuals aged 18 and above, enhancing fraud monitoring and data integrity, while the introduction of the Nigerian Overnight Financing Rate (NOFR) improves transparency, price discovery, and monetary policy transmission in the money market. In parallel, the Central Securities Clearing System Plc (CSCS’s) transition to a value-based, tech-driven model signals capital market modernization, though higher transaction costs may weigh on retail participation in the near term. Reflecting these developments, the IMF maintains a cautiously optimistic outlook for Nigeria, projecting 2026 growth at 3.10% (previously. 3.30%) and 2027 growth steady at 3.20%, supported by reform momentum and improved oil output, but still constrained by inflation, FX pressures, and structural inefficiencies.

The Naira appreciated by ₦12.55 (-0.93%) week to date, trading within the range of $/₦1,356.19 and $/₦1,343.64 in the Nigerian Foreign Exchange Market (NFEM), while posting a ₦13.25 (-0.98%) week-on-week gain and closing at ₦1,343.64 (from ₦1,356.89 the previous week). Foreign reserves showed a mild softening at $48.65 billion (-1.08%) as of April 16, 2026, alongside a marginal decline in blocked funds to $737.59 million (-0.75%), keeping the blocked reserve ratio at 1.52%, displaying a mildly firmer currency backdrop but with lingering external shocks and FX liquidity.

The NGX All-Share Index (ASI) sustained a broadly bullish trajectory during the week, with market capitalization remaining above ₦131.00trn. The index opened at 204,487.85 on Monday, climbed to a peak of 211,900.61 on Thursday, advancing further to close at 217,167.55 on Friday, with market cap settling at ₦140.02trn. Market breadth remained positive, peaking at 1.88x and closing strong at 1.48x, despite a midweek dip to 0.93x that signalled brief profit-taking. Gains were led by Aradel, Airtel Africa, NAHCO, Seplat, and MTNN, while BuaCement, GTCo, and Nestle lagged behind. Notably, Seplat crossed the ₦10,000 mark per share, reflecting an impressive +80% YtD performance. Overall, the ASI advanced by 6.20% WtD (12,679.70 points), 6.56% WoW (13,376.37 points), increasing year-to-date gains to +39.56%.

The week ending April 17, 2026, was characterized by a cautious relief rally across global markets, as a 10-day Israel–Lebanon ceasefire and progress in U.S.–Iran peace talks eased geopolitical risk premiums and supported risk sentiment. China reinforced the tone with stronger-than-expected Q1 GDP growth of 5.0% year-on-year (vs. 4.8% consensus), driven by a 14.7% surge in exports and 6.1% industrial output, though softer retail sales (2.4%) and a 5.4% unemployment rate highlighted lingering domestic fragilities. Equities rallied broadly: the S&P 500 reached a record 7,126.06 (+1.2%), the Nasdaq advanced 1.52% to 24,468.48, and the Dow rose 1.79% to 49,447.43, while Japan’s Nikkei 225 briefly touched 59,518.34 before easing to 58,868.41; China’s Shanghai Composite held at 4,050.43 (-0.1%), with Hong Kong’s Hang Seng Index also advancing on improved regional risk appetite at 26,160.33 (-0.89%). In South Korea, the KOSPI extended gains but declined by 0.55% at 6,191.92 in line with broader Asian equities amid the easing geopolitical premium and improved global growth sentiment. In Europe, the FTSE 100 rose 0.73% to 10,667.63, alongside Germany’s DAX 40 at 24,702.00 (2.27%). In fixed income, focus centred on the UK Debt Management Office’s record £15bn gilt syndication at a 4.9158% yield, attracting £148bn in demand, before secondary 10-year yields eased to around 4.77% as oil prices slipped back below $100, helping to temper inflation concerns despite ongoing risks tied to the Strait of Hormuz blockade.

In the week ended April 17, 2026, commodities traded in a highly volatile but ultimately softening correction phase following earlier geopolitical-driven spikes. Gold oscillated around the $4,700–$4,850/oz range, briefly dipping on Monday’s risk escalation before recovering as US–Iran ceasefire optimism strengthened, ultimately ending at $4,833.56/oz and posting a modest weekly gain of 2.5% as easing inflation expectations and a weaker dollar offset earlier risk-off pressure. In energy markets, both Brent and WTI crude initially surged above $100/bbl. on supply shock fears triggered by the Strait of Hormuz blockade, before steadily retreating through the week as ceasefire progress and diplomatic signals eased disruption concerns; by Friday, Brent slid back below ~$84/bbl. while WTI eased at $90.38/bbl. Overall, the week reflected a clear transition from acute geopolitical risk pricing to partial de-escalation, with oil correcting sharply from early-week peaks while gold remained supported but capped by improving risk sentiment and softer inflation expectations.

The near term remains liquidity-supported but inflation-pressured if no altering event occur, with over ₦2.60trn in expected inflows (FGN 16.245% Apr. 2037 coupon of ₦145.98bn, NTBs ₦758.32bn, and OMOs ₦1.70trn) set to cushion money markets and sustain short-term stability. However, rising MoM inflation momentum versus slower YoY adjustment signals building underlying price pressure, likely keeping policy stance cautious and yields mildly biased upward (10–25bps repricing risk). Interbank liquidity should remain strong, FX broadly range-bound, while fixed income trades defensively with selective duration positioning rather than outright risk-on bets. Highlighting a “stable but not complacent” policy and investment backdrop.

By: Sandra A. Aghaizu

Liquidity flows like a generous bid,

₦2.6 trillion easing the spread.

Coupons and bills drift into the stream,

Supporting the market, steady, not free.

Yet inflation ticks, a quiet repricing,

MoM whispers where YoY is disguising.

Yields edge upward, a cautious tone,

No full risk-on, just positions well-known.

Interbank calm, FX range confined,

A balanced book, alert in mind.

For in still waters, signals prepare,

Stability holds, but trade with care.

Subscribe now to keep reading and get access to the full archive.