May 2026, Edition 3

The week ending May 15, 2026, showed mixed market signals in Nigeria’s fixed-income market. T-bills eased on strong demand, FGN bond yields edged modestly, and Eurobonds weakened on global risk-off sentiment. Inflation data revealed a split dynamic, with headline CPI rising to 15.69% YoY, while core inflation slowed to 15.86% YoY (1.03% MoM), suggesting that food and supply-driven pressures remain drivers.The DMO listed a₦47.3bn green bond and announced a ₦600bn FGN bond offer volume for the May 2026 bond auction. Nigeria’s oil output improved to ~1.66mbpd, FX remained stable around $/₦1,370, reserves rose to $48.54bn, and equities stayed resilient. Amidst a backdrop of sweeping regulatory reset, tighter compliance enforcement, and ongoing FX liberalisation, the financial system continues to recalibrate toward stronger governance, transparency, and capital resilience. Globally, a hotter US inflation at 3.8% (highest since May 2023) and Producer Price Index (PPI)at 6.0%, with 10Y yields at 4.6%, alongside leadership shifts at the U.S. Federal Reserve, Bank of Japan (BoJ) tightening signals, weak Eurozone growth, and surging oil prices, all reinforced a higher-for-longer rates regime and broad risk-off tone across global markets. Week-on-week, Brent crude and West Texas Intermediate (WTI) closed at $109.03/bbl.(+4.63%), and $105.04/bbl. (+7.56%), while goldat $4,559.47/oz (-3.61%).

Interbank liquidity stayed strong through the week, opening at ₦ 4.92trn surplus, peaking at ₦ 6.89trn, and closing at ₦5.83trn (+19.17 % WTD). Money market rates were broadly stable, with the Open Repo Rate (OPR) at 22.00%, the Overnight rate (O/N) opening at 22.21%, and peaking at 22.24%.In the FX market, the Naira traded between$/₦1,367.00 and $/₦1,377.90, before closing at $/₦1,371.04 on Friday.

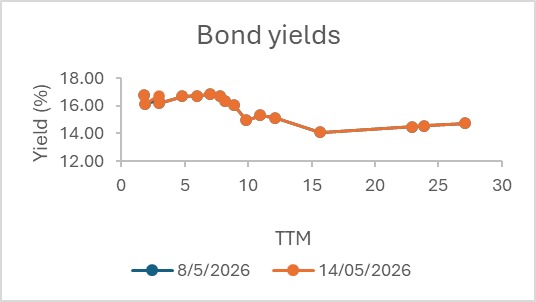

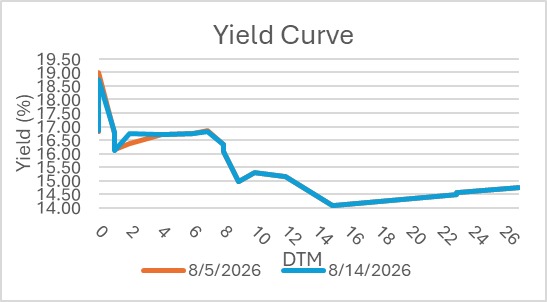

The fixed-income secondary market delivered a mixed performance over the week. T-bills attracted strong demand across several maturities, particularly observed at the 1-year (06-May-27, 17-Dec-26, and 23-Jul-26)bills, while pockets of selling interest emerged in select tenors, including the 25-Mar-27, 03-Dec-26, and 21-Jan-27 bills. The FGN bond yields inched higher by roughly 10 basis points week-on-week, with light activity at the long end and trading skewed toward the 2026–2035 segment; selling pressure featured in the Apr-29, Nov-28, and Jan-35 bonds, even as demand supported mild yield declines in parts of the 2027 and 2030 curve. Eurobonds weakened broadly as global risk sentiment reduced, leading to across-the-board sell-offs, with notable downside moves in the Sep-33, Feb-32, and Feb-38 maturities.

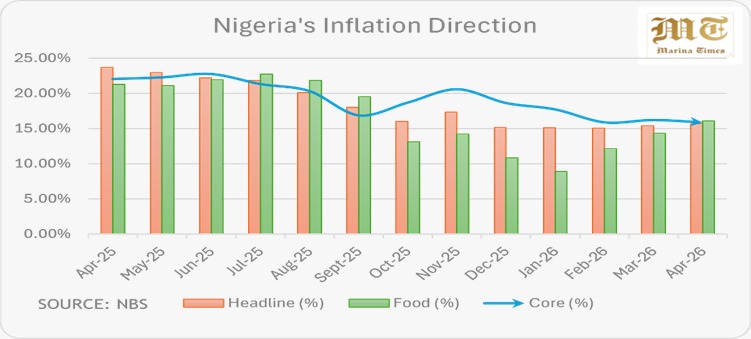

According to the National Bureau of Statistics(NBS), Nigeria’s April 2026 CPI report indicates a split inflation picture. Headline inflation rose to 15.69% YoY, masking a notable moderation in underlying systemic price pressures. While inflation accelerated for the second consecutive month, the increase remains heavily concentrated in the food basket, with food inflation rising to 16.06%, reflecting persistent supply-chain bottlenecks, logistics costs, and seasonal pressures. In contrast, core inflation moderated sharply to 15.86% YoY and slowed to 1.03% month-on-month, signalling easing demand-side and monetary-driven inflationary pressures. The variance reinforces the view that Nigeria’s inflation challenge is becoming increasingly supply-driven rather than broad-based, supporting expectations of a cautious Central Bank of Nigeria (CBN), with hawkish-to-neutral stance as policymakers assess whether sustained moderation in core inflation can eventually steer headline inflation back toward its long-term disinflation path.

Policy and funding developments were notable during the period, highlighted by the Debt Management Office’s (DMO) listing of a ₦47.3bn Green Bond on May 13, reinforcing the gradual expansion of ESG-aligned sovereign funding instruments. At the same time, the DMO also issued a circular for ascheduled May 2026 FGN Bond auction to be held on May 18, 2026, with a combined ₦600bn (equal split) for re-opened papers [the 22.60% FGN Jan 2035 (10-year) and 16.25% FGN Apr 2037 (20-year)], a decline of 14.3% in offer volume from previous sale and exclusion of the 2032 paper from issuance, signaling continued reliance on the domestic bond market for medium- to long-term financing. In parallel, regulatory developments from the National Pension Commission (PenCom) introduced a one-off dispensation permitting Pension Fund Administrators to participate in the proposed Initial Public Offering (IPO) of Dangote Petroleum Refinery & Petrochemicals under defined governance and risk controls, temporarily waiving some select entry requirements, emphasising a controlled broadening of institutional participation in domestic capital markets while maintaining strict fiduciary safeguards.

At the same time, the banking sector witnessed a broad regulatory and operational reset as the Central Bank of Nigeria (CBN) intensified oversight across banking, foreign exchange, and non-interest finance segments. The apex bank warned non-interest financial institutions against rising governance, Shariah non-compliance, operational, and fintech-related risks that could erode confidence in Nigeria’s expanding Islamic finance ecosystem, while reaffirming efforts to deepen financial inclusion and ethical funding through stronger regulatory engagement. Simultaneously, its enforcement of dormant account disclosure guidelines led Access Bank, Union Bank of Nigeria, Stanbic IBTC Bank, and Fidelity Bank to publish over 321,000 inactive accounts, exposing the lingering impact of SME failures, abandoned businesses, weak customer engagement, and concerns around privacy and bureaucratic account recovery processes. In parallel, it launched the 4th Edition FX Manual, effective June 1, 2026, raising the allowable import advance payment limit to 30% (prev. 15%), liberalising several FX processes, and strengthening transparency measures to boost liquidity, investor confidence, and market efficiency amid growing autonomous FX inflows. Against this backdrop, Sterling Financial Holdings Company Plc reported robust earnings and a balance sheet expansion, with total assets surpassing ₦4 trillion in Q1 2026 following strong profit growth and recapitalisation, highlighting resilience and a capital-strengthening trend within Nigeria’s financial sector.

Nigeria’s oil production increased in April 2026, with reported output rising to about 1.66 million barrels per day (crude oil and condensates combined), reflecting a month-on-month improvement from March levels and bringing production close to the country’s 1.5 million bpd OPEC quota on a crude-only basis. Crude oil output was estimated at roughly 1.49 million bpd, while condensates contributed the balance, lifting total liquid production for the period. The improvement signals continued gradual recovery in upstream performance, supported by relatively stronger field uptime and output across key producing assets, even as operational disruptions and security risks remain intermittent constraints. Overall, the data points to a sustained but fragile production rebound, with Nigeria maintaining output levels broadly in line with its near-term OPEC obligations while still facing structural volatility in meeting higher output targets consistently.

The Naira gained ₦2.12 (-0.15%) week-to-date (WTD), largely trading at the $/₦1,370.00b and in the Nigerian Foreign Exchange Market (NFEM), marking a week-on-week loss of ₦9.64 (+0.71%), and settled at $/₦1,371.04 (WoW ₦1,361.40). Foreign reserves improved to $48.54bn (+0.37%)as of May 14, 2026, with blocked funds easing to $707.64m (-1.95%), while the blocked reserve ratio moderated at 1.46%. Indicating relatively stable FX conditions amidst external pressures.

The Nigerian equities market traded mixed but broadly resilient during the week ended May 15, 2026, as the NGX ASI fluctuated amid profit-taking and shifting investor sentiment. The benchmark index opened at 250,485.54 points, rallied to an intra-week high of 253,411.67 points, before easing to close at 250,330.92 points (-0.06% WtD) and +2.27% WoW, with YtD higher at +60.87%. Market capitalisation increased from ~₦154.46trn to ₦162.00trn. Despite the late-week pullback, market breadth remained firmly positive, ranging from 1.23x to 2.57x, reflecting sustained buying interest across the market. Trading activity was largely supported by mid- to large-cap tickers, even as gains in the banking index continued to provide directional support for the broader market across the core sectoral indices. Largely, the performance suggests investors maintained selective bullish positioning while cautiously rebalancing portfolios.

The global financial market was defined by a hawkish regime shift expectation and surging yields as a “hot” US April 2026 Inflation at 3.80%and PPI print of 6.0% YoY, driven by a 7.8% monthly energy spike, crushed hopes for near-term rate cuts and propelled 10-year Treasury yields to a one-year peak of ~4.6%. In a historic leadership transition, Kevin Warsh was confirmed as Fed Chair following Jerome Powell’s exit, while the Bank of Japan’s Kazuyuki Masu signalled an “imminent” hike to 1.0% to defend the yen against rising producer prices (up 4.9% YoY). The Eurozone contributed to the cautious outlook with Q1 2026 data showing a marginal 0.1% increase in both GDP and employment, alongside a sharp upward revision of inflation forecasts to 2.6% for the year. This tightening bias, compounded by oil price volatility amid geopolitical tensions, triggered a global retreat in equities: with the S&P 500 closing at 7,408.50 (+0.14% WoW), the Nasdaq Composite easing to 26,255.41 (-0.08% WoW), and the Dow Jones Industrial Average at 49,526.17 (-0.17% WoW). Across Europe, Germany’s DAX 40 closed at 23,950.57 (-1.59% WoW) while the FTSE 100 settled at 10,195.37 (-0.37% WoW). Meanwhile, Asian markets eased with Japan’s Nikkei 225 at 61,409.29(-2.08% WoW), while China’s Shanghai Composite Index ended at 4,135.39 (-1.07% WoW), Hong Kong’s Hang Seng Index at 25,962.73 (-1.63% WoW), and South Korea’s KOSPI settled at 7,493.18 (-0.06% WoW). The UK Gilt yields climbed above 5.15%, and US indices tumbled over 1%. Despite China’s Q1 GDP resilience at 5.0%, the interplay of soaring borrowing costs and “higher-for-longer” central bank rhetoric across the US, Europe, and Asia has shifted market sentiment toward defensive positioning as the era of cheap liquidity firmly recedes.

During the period, African financial markets traded in a broadly risk-sensitive global environment, with commodity price movements, particularly in energy, acting as a key driver of regional sentiment and reinforcing inflation pressures for import-dependent economies while supporting external positions in commodity exporters. Equity performance was mixed across regions: South Africa showed relative resilience on cyclical and resource-sector strength, Egypt maintained stable momentum supported by ongoing macroeconomic reforms, Kenya remained subdued amid tight financial conditions and fiscal consolidation pressures, and Ghana’s outlook was anchored on continued engagement with multilateral financing frameworks despite persistent FX constraints. Currency markets remained range-bound as central banks prioritised exchange-rate stability under elevated global interest rates. Overall, African markets continued to reflect a dual dynamic of country-specific divergence alongside shared exposure to global rate conditions, capital flow sensitivity, and commodity volatility.

Global commodities markets were dominated by escalating Middle East tensions, as the prolonged disruption of the Strait of Hormuz intensified supply fears, market volatility, and inflation concerns. Crude oil prices surged sharply, with Brent crude climbing from about $104bbl. at the start of the week to above $109/bbl. Friday, while WTI advanced from roughly $98/bbl. to above $105/bbl., posting strong weekly gains amid tightening inventories, reduced Saudi output, and warnings from the IEA that the oil market could remain severely undersupplied until October, even where hostilities ease. Gold initially rallied to near-record highs above $4,730/oz on safe-haven demand but later reversed sharply, ending the week around $4,560/oz as hotter-than-expected US inflation data, rising Treasury yield expectations, and fading hopes for Federal Reserve rate cuts strengthened the dollar and pressured bullion prices.

The near term is set to be highly eventful, from the May 2026 FGN Bond Auction to the NTB auction with a combined offer of ₦600bn and ₦650bn, respectively, in addition to the CBN’s 305th MPC meeting decision and expected inflows of over ₦2.71trn. System liquidity is poised for episodic actions with aggregates from FGN bond coupon payments of ₦17.87bn [for 8.50% Nov. 2029 and 12.49% May 2029] and 19.75% FGN Sukuk May 2032 (₦29.63bn) paper, as well as maturing OMO and NTBs of ₦2.25trn and ₦634.47bn, alongside fresh OMO auction(s). Market focus will centre on the outcome of auctions and the policy rate decision, following the uptick in inflation in addition to global macroeconomic pressures and geopolitical tensions.

By: Sandra A. Aghaizu

Money moved like rain before the storm,

pouring through the veins of the market.

Old bonds returned home like weary travelers,

their pockets heavy with interest and time.

The banks stood watching the tide rise,

while the central bank held the gate

like a cautious lighthouse keeper

measuring inflation against the wind.

And investors,

like fishermen beneath a restless sky,

cast their nets carefully,

waiting to see where the current

would carry tomorrow’s wealth.