Nigeria’s financial markets are entering a more nuanced phase where liquidity is no longer the sole driver, and discipline is quietly taking over. Across fixed income, equities, FX, and even commodities-linked sentiment, investors are recalibrating positions in response to rising inflationary risks, policy signals, and global shocks. While the surface suggests stability, beneath lies a market actively repricing risk, selectively extending duration, narrowing equity participation, and cautiously absorbing supply; all within an environment shaped by volatility. The secondary market traded mixed and largely range-bound, with mild bearish pressure pushing yields slightly higher across T-bills (15.70%–16.10%) and FGN bonds (up 10–15bps to mid-16%), while OMOs remained elevated near upper-19%. Eurobonds showed a mildly flattening curve, with stable short-end rates, easing mid-tenors, and slightly compressed long-end yields, reflecting a selective risk appetite. Strong liquidity continued to drive demand in OMO and NTB auctions, especially at the long end, reinforcing a yield-sensitive but cautiously supportive market with a near-term floor forming across fixed income. Week-on-week, oil closed with a gain, with Brent crude and West Texas Intermediate (WTI) at $104.70/bbl. (+15.84%), and $93.50/bbl. (+11.59%), while gold was at $4,724.94/oz (-2.25%).

Interbank liquidity opened on Monday at a ₦3.57trn surplus, mildly softened yet steady at an above ₦3.60trn base during the week, and closed at ₦3.97trn on Friday, a WTD gain of 11.31%. Money market rates were relatively stable, with the Open Repo Rate (OPR) steady at 22.00%, while the Overnight rate (O/N) opened at 22.23%, peaked at 22.29% before closing at 22.20%. In the currency market, Naira traded between $/₦1,340.00 and $/₦1,361.50, before closing at $/₦1,358.44 on Friday.

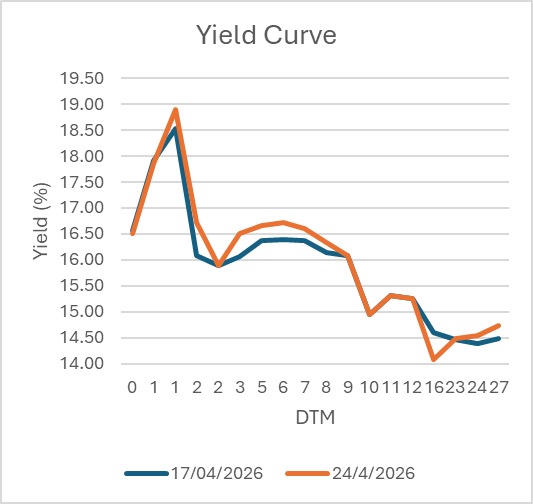

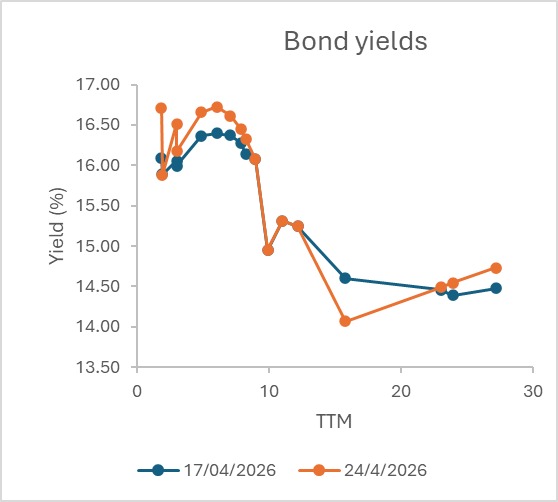

The secondary market traded in a mixed tone and was largely range-bound with a mild bearish momentum, and slight uptick in yields across the curve. Treasury bills remained within the 15.70%-16.10% levels following the recent auction, OMOs stayed sticky around the upper-19% levels, while FGN bonds saw average yield inch up by 10-15bps to mid-16% range (with selective preference for the mid and long end of the curve). The cautious trend, rather than broad sell-offs, echoed a defensive positioning.

Nigeria’s Eurobond curve remained bullish but mildly flattened over the period (Apr. 15 – 23, 2026), reflecting improved investor sentiment and selective duration demand. Short-term yields (2027–2029) stayed compressed and stable around ~5.68%–5.80%, indicating strong demand for lower-risk tenors, while mid-tenors (2030–2034) traded in the ~6.15%–7.45% range, easing slightly as investors sought yield pick-up with manageable risk. Long-term bonds (2036–2051) remained elevated at ~7.28%–8.20%, though with modest compression into the close, indicating renewed appetite for duration despite persistent sovereign risk premia, ultimately pointing to a cautiously improving credit outlook.

The April 21, 2026, OMO auction reflects a liquidity-heavy but increasingly yield-sensitive market, with total demand of ₦2.22trn (~3.7x the ₦600bn offer) skewed sharply toward the 7-day and 140-day tenors, while the 91-day saw weak participation, highlighting a barbell positioning strategy, short-term liquidity parking, and selective duration extension. Stop rates held steady, particularly at the 7- and 140-day, signalling a deliberate CBN effort to re-anchor yields without choking liquidity. The strong uptake of system liquidity in pursuit of real returns, while the mid-curve rejection persists, suggests limited conviction. Overall, the outcome points to a controlled regime in which pricing is more disciplined, with steady pressure on yields and a developing curve kink that is likely to persist in the near term.

AUCTION DATE | TENOR | OFFER (₦‘B) | BIDS (₦‘B) | TOTAL SALE (₦‘B) | STOP RATES (%) | PREVIOUS TENOR STOP RATES (%) |

| 7-DAY | 200.00 | 884.00 | 684.00 | 21.9000 | 21.9000 |

91-DAY | 200.00 | 87.00 | 21.00 | 19.8700 | 19.8800 | |

140-DAY | 200.00 | 1,246.04 | 1,211.00 | 19.9100 | 19.9100 |

The second NTB auction in April 2026 (April 22) underlines sustained investor preference for duration, supported by elevated system liquidity, with demand strengthening along the curve, as Bid-to-Cover Ratios rose from 1.13x (91-day) to 2.26x (182-day) and 2.81x (364-day). Despite only moderate-to-strong subscription levels on the mid- and long-tenors, the DMO maintained a selective stance, allocating just 37.8% of total bids, with a high skew in sales of the 364-day instrument. Stop rates were steady, with effective yield unchanged at 16.61% (91-day), 17.61% (-1bp, 182-day), and 19.32% (364-day), reflecting anchored yield expectations. Notably, the bid distribution suggests firm resistance around the 15% levels, reinforcing a near-term floor for rates, amid persistent liquidity and cautious policy signals.

AUCTION DATE | 22-04-2026 | 22-04-2026 | 22-04-2026 |

MATURITY DATE | 23-07-2026 | 22-10-2026 | 22-04-2027 |

TENOR | 91-DAY | 182-DAY | 364-DAY |

OFFER (₦) | 100,000,000,000 | 100,000,000,000 | 550,000,000,000 |

SUBSCRIPTION (₦) | 72,731,914,000 | 172,081,003,000 | 2,119,119,219,000 |

ALLOTMENT (₦) | 64,480,912,000 | 76,235,371,000 | 753,447,572,000 |

BID RANGE (%) | 15.0000 – 16.1400 | 15.3000 – 17.0000 | 15.0000 – 19.4200 |

STOP RATES (%) | 15.9500 | 16.1900 | 16.1990 |

PREVIOUS STOP RATES (%) | 15.9500 | 16.1900 | 16.1990 |

The Debt Management Office (DMO) announced the April 2026 FGN Bond Auction with a total offer of ₦700 billion (-6.7% from March 2026) scheduled for April 27, 2026, with a 3:1:3 ratio of three reopened papers (17.945% FGN AUG. 2030, 17.95% FGN JUN. 2032, and 22.60% FGN JAN. 2035). The offer reflects a clear duration-weighted funding strategy, with heavier allocation to the 5- and 10-year tenors when compared to the 7-year tenor, indicates the DMO’s intention to balance near-term refinancing needs with long-term debt extension. Overall, the auction is likely to attract strong demand from institutional investors seeking attractive real returns, though pricing dynamics will hinge on system liquidity with a bias toward slightly higher yield demands at the long end given duration risk and supply concentration.

Nigeria’s macro and market landscape reflects a coordinated policy push to stabilize key sectors while unlocking long-term growth. The proposed $516m external financing for the Sokoto–Badagry Superhighway signals continued reliance on concessional borrowing to drive infrastructure-led connectivity and trade efficiency, albeit with rising debt service considerations, while the government’s intervention in the aviation sector, via planned debt waivers and potential tax/levy reductions, highlights urgent fiscal support to prevent systemic disruption from the Jet A1 price shock. At the same time, structural capital market reforms by the Nigerian Exchange Limited, including extended trading hours, aim to deepen liquidity and attract foreign participation following the FTSE reclassification, reinforcing market efficiency. On the industrial front, expansion plans by Aliko Dangote to scale refining capacity and replicate infrastructure across Africa underline a strategic shift toward energy self-sufficiency and export capacity. While the proposed initiatives collectively support growth, improving capital access, reducing cost inefficiencies, and ensuring disciplined debt management will be critical to sustain investor confidence and translate policy momentum into broad-based economic resilience.

The Naira edged lower by ₦8.76 (+0.65%) week-to-date, trading between $/₦1,349.67 and $/₦1,358.44 in the Nigerian Foreign Exchange Market (NFEM), while still recording a marginal week-on-week depreciation of ₦14.80 (+1.10%), closing at $/₦1,358.44 (WoW ₦1,343.64). Foreign reserves softened to $48.45 billion (-0.41) as of April 23, 2026, with blocked funds easing slightly to $733.00 million (-0.62%), keeping the blocked reserve ratio at 1.51%. Overall, FX conditions remained relatively stable but continued to reflect underlying liquidity pressures and external shocks.

The NGX All-Share Index (ASI) trended higher over the week, rising from 218,115.07 to close at 225,724.33, as market capitalization crossed ₦140 trillion and settled at ₦145.55 trillion. However, market breadth remained weak, falling to 0.56x, briefly turning positive at 1.03x, and closing at 0.73x, highlighting a top-heavy rally driven by a few large-cap financial stocks. This divergence suggests that while liquidity is strong and banking stocks continue to attract interest, overall market participation is limited, making the rally fragile and narrowly supported. Gains were led by Unilever, Wapco, ETI, and NAHCO, while profit-taking was seen in Stanbic, Interbrew, and MTNN. Overall, the ASI gained 3.49% WtD (7,608.56 points), 3.94% WoW (8,556.78 points), bringing year-to-date returns to +45.05%.

The week ended April 24, 2026, was defined by market consolidation and renewed caution as the U.S.–Iran conflict intensified, disrupting shipping through the Strait of Hormuz and keeping energy prices elevated, thereby prompting the European Commission to unveil its 44-action “AccelerateEU” energy plan to bolster domestic resilience. Against this backdrop of heightened geopolitical risk, the Bank of England maintained its Bank Rate at 3.75% ahead of its upcoming April 30th decision, while South Africa’s annual consumer price inflation edged up to 3.1% in March, reflecting the broader pass-through of global supply-side pressures. Consequently, global equities pulled back from previous highs: in the U.S., the S&P 500 fell to 7,165.08 (+0.80), the Nasdaq Composite index inched to 24,836.60 (+1.63%), and the Dow Jones Industrial Average eased to 49,230.71 (-0.16%). Asian markets followed a similar upward trend, with Japan’s Nikkei 225 easing to 59,716.18 (+2.10%), China’s Shanghai Composite at 4,079.90 (-0.33%), Hong Kong’s Hang Seng Index increasing to 25,978.07 (+0.24%), and South Korea’s KOSPI flat at 6,475.63. In Europe, the FTSE 100 traded down to 10,379.08 (-0.67%), while Germany’s DAX 40 retreated to 24,128.98 (-0.11%), as investors prioritized defensive positioning amidst the persistent shipping blockade and volatile macroeconomic outlook.

In the week ending April 20, 2026, the commodities market reflected a pronounced inflationary shock, driven by escalating tensions in the Strait of Hormuz, with energy markets rallying sharply while gold weakened under rate pressure. Crude oil posted strong gains, with WTI rising from an intra-week low near $88/bbl. to a peak above $97/bbl. before closing at $93.50/bbl., while Brent climbed from roughly $95/bbl. to a high above $106/bbl., settling near $104.70/bbl., marking weekly gains of over 16–17% amid severe supply disruptions and constrained shipping flows. Conversely, gold remained under pressure, trading between a weekly high of about $4,800/oz and a low near $4,692/oz, before closing at $4,724.94/oz, down roughly 3% on the week and nearly 10% since the onset of the conflict, as elevated energy prices intensified inflationary concerns and reinforced expectations of a tighter monetary policy, eroding the appeal of a non-yielding bullion.

Looking ahead, near-term markets are likely to remain in a balanced tug-of-war. Liquidity should stay supportive, driven by over ₦979.67bn in inflows from FGN coupon payments (₦75.68bn on 14.55% Apr. 2029, ₦53.35bn on 12.50% Apr. 2032, and ₦131.64bn on 14.80% Apr. 2049) alongside ₦719.00bn in OMO maturities. However, rising supply and inflation risks are expected to keep yields biased upward, especially at the long end. Equities may extend gains but remain selective and top-heavy, while FX stability faces mild pressure from external shocks. Overall, the April 2026 FGN Bond Auction is likely to clear in the high-15% range, with potentially uneven allotments despite stronger oil price support.

By: Sandra A. Aghaizu

The market walks a narrow spread of doubt,

liquidity still clears, but bids grow thin.

Like a trader watching flickering charts,

waiting for a breakout beyond resistance.

Oil futures burn in distant waters,

each barrel marked up by risk premium.

Volatility ticks beneath steady candles,

a hedged storm in leveraged silence.

Capital rotates with cautious intent,

risk-off flows into safe-haven trades.

And in this pause, this priced-in breath,

the world is not breaking, just repricing its books.

Subscribe now to keep reading and get access to the full archive.