Financial markets navigated a week defined by policy reset, liquidity repricing, and shifting global macro conditions, as investors balanced tightening monetary settings against emerging signs of external stability and selective growth opportunities. In Nigeria, fixed-income markets remained volatile amid active liquidity sterilisation, elevated yield conditions, and cautious duration positioning, while stronger external buffers, improved trade dynamics, and a relatively stable Naira supported broader market resilience. Equity sentiment stayed constructive but increasingly selective as investors rotated toward quality and earnings visibility. Globally, markets contended with oil price swings, renewed inflationary concerns, and expectations of higher interest rates, reinforced by hawkish signals from major central banks. Across Africa, improving growth momentum, selective policy easing, and expanding regional capital market integration continued to shape investment flows, highlighting a market environment increasingly driven by disciplined capital allocation, policy credibility, and long-term positioning. Commodities closed week-on-week (WoW), with Brent crude and West Texas Intermediate (WTI) at $87.10/bbl. (-6.10%) and $84.42/bbl. (-6.26%) respectively, while gold declined to $4,218.50/oz (-2.85%).

Interbank liquidity remained robust throughout the week, opening at a ₦4.50 trillion surplus, peaking at a close of ₦4.71 trillion (+4.55% WTD) on Thursday. Money market rates were stable, with the Open Repo Rate (OPR) at 22.00% and the Overnight (O/N) rate at 22.16%, (+0.12bps). In the FX market, the Naira traded within a range of $/₦1,359.00 and $/₦1,365.50, before settling at $/₦1,363.83 on Thursday.

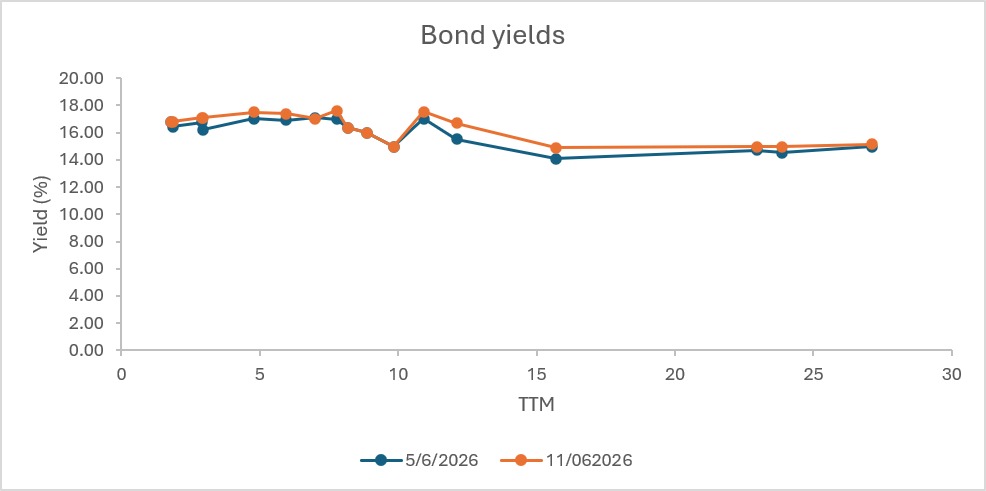

Nigeria’s fixed-income market exhibited heightened volatility with bearish sentiment across both money market, FGN Bonds and Eurobonds, driving yields up; 16.10% – 16.62%, 18.80% – 20.15%, 16.50% – 17.70%, and 6.82% – 6.86% range for the T-bills, OMO bills, FGN bonds, and Eurobonds, respectively. Indicating a sell-off driven week characterised by offshore flight/dumping, and persistent repricing pressure at the belly and long end of the curve.

Liquidity Pulse: The CBN’s OMO auction on 8 June 2026 reflected a selective but duration-skewed demand profile, with weak appetite for the short 8-day bill (0.28x subscription) contrasted by strong oversubscription in the 134-day tenor (5.35x), with a 35bps upward move and unchanged stop rate, respectively, indicative investor preference for mid-to-long duration instruments amid expectations of stable-to-elevated yields. Despite the mixed tenor dynamics, overall liquidity absorption was robust, with total subscriptions and allotments reaching ₦1.69tn against an offer of ₦600bn, and full clearance of the auction. The outcome emphasized sustained system liquidity pressures and continued investor demand for attractive yields.

AUCTION DATE | TENOR | OFFER (₦‘B) | BIDS (₦‘B) | TOTAL SALE (₦‘B) | STOP RATES (%) | PREVIOUS TENOR STOP RATES (%) |

| 8-DAY | 300.00 | 85.00 | 85.00 | 21.8900 | 21.5400 |

134-DAY | 300.00 | 1,604.50 | 1,604.50 | 20.0200 | 20.0200 |

The Debt Management Office (DMO) revised its offer for the Wednesday, June 17, 2026 scheduled NTB auction, increasing total offering by ₦550bn (a 220% rise) to ₦1.00tn from ₦450bn. The adjustment reflects a shift in tenor composition, with the 91-day bill reduced by 33.3% to ₦100bn from ₦150bn, while the 182-day bill was raised by 100% to ₦100bn from ₦50bn, and the 364-day bill was significantly increased by 220% to ₦800bn from ₦250bn, indicating a strong bias toward longer-dated instruments in the auction structure. The revision points to active debt management aimed at optimizing refinancing costs and further soaking up liquidity in the system. Importantly, NTBs are now subject to withholding tax (WHT) deduction, which reduces investors’ effective returns, even as the instruments remain attractive for yield locking in a still-high-interest-rate environment.

Nigeria’s latest CBN indicators present a consistent picture of an economy balancing macroeconomic stabilisation against weakening real-sector activity. While the Composite Purchasing Managers Index (PMI) improved marginally to 49.6 in May 2026 from 49.4, it remained below the 50-point threshold for a second consecutive month, signalling continued contraction driven by weak services and industrial activity despite sustained agricultural expansion. Softer new orders, slower supplier deliveries, and declining inventories reflected subdued business conditions, even as employment showed modest improvement. Thereby aligning with findings from the CBN’s report on the May 2026 Household Expectation Survey (HES), Inflation Expectation Survey (IES), and Business Expectation Survey (BES), which collectively reflect continued firm monetary and liquidity conditions aimed at containing inflation and supporting FX stability. Although stronger FX inflows and reserve accumulation have improved external buffers and business planning confidence, elevated financing costs, persistent inflation, weak demand, and rising operating expenses, particularly energy, transportation, and raw materials, continue to constrain investment and business expansion. Overall, current policy settings appear to support external price stability, but at the cost of softer private sector momentum, sustained high fixed income yields, and a delayed recovery in credit growth and broader economic activity.

The CBN also proposed a strict regulatory overhaul mandating that financial holding companies operate as purely non-operating entities, completely barred from the daily management or lending decisions of their subsidiaries. The framework requires parent companies to maintain a minimum 51% equity stake in each unit and hold regulatory capital of at least 20% above the combined minimum requirements of their subsidiaries. Furthermore, it strictly bans using customer deposits for intra-group lending, proprietary trading, or debt servicing, while shifting the direct ownership of foreign subsidiaries to the parent holding company to simplify corporate structures.

According to Nigeria’s National Bureau of Statistics (NBS) Report, Nigeria’s Q1 2026 trade data signals a stronger external position, with the merchandise trade surplus surging 341% quarter-on-quarter (QoQ) to ₦7.55trn, driven by higher crude and refined petroleum exports alongside a sharp contraction in imports, particularly petroleum-related imports. Total exports expanded to ₦21.17tn and represented 60.9% of trade, while imports declined 18.17% QoQ to ₦13.62trn, reflecting improved FX efficiency, lower import dependence, and effects of ongoing domestic energy substitution. However, the structure of trade remains heavily concentrated, with mineral products accounting for 85.8% of exports, with Europe as the leading export endpoint, while crude oil alone contributed 52.9%, highlighting continued vulnerability to commodity price and production shocks. Near term, the data is supportive of Nigeria’s external reserves, Naira stability, current account strength, and fiscal liquidity through improved oil-linked revenues, while potentially easing pressure on monetary tightening. Nonetheless, weak agricultural exports and limited growth in manufactured exports emphasize that structural diversification remains insufficient to sustain long-term trade resilience and broad-based economic expansion.

The United Capital Group’s acquisition of investment banking licences in Ethiopia and Rwanda highlights a strategically significant expansion that strengthens its position as a leading pan-African financial services platform. Notably, the Ethiopian approval establishes United Capital as the first foreign institution authorised to deliver investment banking services in the market, including financial advisory, securities brokerage, and portfolio management, thereby providing early-mover access to one of Africa’s most promising frontier capital markets. The expansion aligns with broader regional reforms aimed at deepening financial market participation and attracting institutional capital. Combined with its recent entry into Rwanda, the development extends United Capital’s operational footprint to 12 African markets and reinforces its long-term strategy of building integrated capital market infrastructure across Africa. From an investment perspective, the move enhances geographic diversification, creates new revenue channels across the advisory and asset management businesses, and positions the Group to benefit from increasing cross-border capital flows and long-term economic formalisation in East and Central Africa.

FCMB Group delivered a strong Q1 2026 performance, emphasizing the effectiveness of its balance sheet optimisation and funding strategy in a high-yield environment. Profit before tax surged 148.39% YoY to ₦87.50bn, while profit after tax rose to ₦76.527bn and gross earnings expanded 26.72% to ₦320.220bn. Growth was primarily driven by a 92.41% increase in net interest income to ₦168.35bn, supported by stronger returns on cash balances and investment securities, lower wholesale funding costs, and continued growth in customer deposits to ₦4.68tn. Although impairment charges (+29.28% from Q1, 2025) and operating expenses increased, FCMB maintained strong operating leverage, with total assets rising to ₦7.96tn and shareholders’ funds surpassing ₦1.1tn. The appointment of Mr. Bismarck J. Rewane as Board Chairman further strengthens the Group’s strategic positioning, reinforcing governance depth and supporting its next phase of growth across banking and financial services.

The Naira steadied around the $/₦1,360.00 band during the week in the Nigerian Foreign Exchange Market (NFEM), with a gain of ₦0.99 (+0.07%) week-to-date (WTD), and ₦1.61 (+0.12%) WoW, before closing at $/₦1,363.83 (WoW ₦1,362.21). Foreign reserves advanced its ascent up the $50bn mark to print at $50.43bn (+0.78%) as of June 10, 2026, leading to a corresponding decline in blocked funds to $672.34m (-0.25%), with an eased blocked reserve ratio of 1.33%(-0.2bps), signifying a relatively stable foreign exchange condition despite external pressures.

The Nigerian equities market traded largely bullish across the first three sessions of the week, with the ASI rising steadily from 243,510.75 on Monday to close at 244,738.74 (WTD +0.50%) on Thursday, lifting ytd returns to 57.27%, driven by sustained interest in large-cap stocks such as MTNN, FIRSTHOLDCO, ACCESSCORP, and AIRTELAFRI, alongside sector-specific gains in banking and selected consumer names. Market activity strengthened sharply on Tuesday, with volume and value nearly doubling (₦57.87bn vs. ₦29.00bn) before moderating on Wednesday (₦38.81bn), while overall breadth weakened across the period (1.29x to 0.76x), indicating growing selectivity and intermittent profit-taking. Sector performance was mixed but generally positive early in the week, led by oil and gas, banking, and insurance gains on Monday and Tuesday, before sentiment softened midweek as banking and industrial stocks came under pressure despite resilience in consumer goods and oil and gas counters. Largely, the market reflects a short-term bullish trend underpinned by earnings-driven momentum and liquidity inflows, but with rising profit-taking and narrowing breadth, suggesting an emerging more cautious, stock-selective positioning phase.

During the week, global financial market was shaped by key macroeconomic developments and heightened oil price volatility during the week. WoW, equities closed mixed: the Nasdaq Composite at 25,888.84 (+0.70%), S&P 500 at 7,431.46 (+0.65%), and the blue-chip Dow Jones Industrial Average at 51,202.26 (+0.66%). Across Europe, Germany’s DAX 40 closed at 24,635.30 (-0.50%), while the FTSE 100 eased at 10,471.72 (+1.00%). Asian markets finished down, with Japan’s Nikkei 225 at 66,020.04 (-0.85%), China’s Shanghai Composite Index at 4,031.51 (+0.09%), Hong Kong’s Hang Seng Index at 24,718.10 (-0.98%), and South Korea’s KOSPI at 8,123.62 (-0.45%). Markets priced a 70% probability of a US Federal Reserve rate hike in December, supported by May 2026 US CPI at 4.2% (highest in nearly three years), PPI at 6.5% y/y (highest since November 2022), and robust employment data (+172,000 jobs). Adding to macro crosscurrents, the European Central Bank (ECB) raised its three key interest rates by 25 basis points, bringing the deposit facility rate to 2.25%, marking its first rate hike in nearly three years to combat resurgent energy inflation despite downgrading Eurozone growth projections to 0.8%. China’s consumer inflation held steady at 1.2% YoY, reflecting subdued domestic demand and easing energy prices, while producer inflation accelerated to 3.9%, supported by stronger industrial activity, rising trade flows, and demand for AI-related technology and machinery. SpaceX has established itself and the 6th largest public company in the world following its historic Nasdaq debut under the ticker SPCX. The historic IPO generated a record-breaking $350bn in total demand, driven by $250bn in institutional orders and over $100bn from retail investors. Offered at a fixed price of $135 per share, the listing successfully raised $75bn at a base valuation of $1.77trn. Following the initial price discovery process, the stock opened for trading at $150 and surged 24% to hit $168 per share. This trading momentum pushed SpaceX’s market capitalization past $2.2trn, permanently solidifying its multi-trillion dollar valuation.

African markets recorded notable fiscal and monetary developments across major economies. Ghana’s Statistical Service announced a robust 6.4% year-on-year GDP expansion for Q1 2026, driven by a 10.7% surge in mining, while the Central Bank of Kenya safely held its benchmark interest rate steady at 8.75% to absorb global fuel shocks despite local inflation rising to 6.7%. Simultaneously, the South African rand rallied to 16.5375 per dollar following a sovereign credit outlook upgrade by Fitch, which also triggered a corporate credit bump for power utility Eskom to B+ with a stable outlook. While its economy grew by 0.5% QoQ in Q1 2026, beating market expectations, with expansion recorded in 9 out of 10 sectors and the financial sector contributing the most to growth, whilst manufacturing contracted. However, the report highlights a key concern as fixed investment declined after two quarters of growth, suggesting weaker capital formation despite overall economic expansion. Although recent fiscal discipline has supported improved investor sentiment, rising geopolitical tensions from the Middle-East conflict are expected to weigh on near-term growth prospects, even as economists maintain a cautiously optimistic medium-term outlook of around 2% growth. In North Africa, the Egyptian Exchange saw heavy foreign buying support even as its benchmark EGX30 index fell slightly to 50,818.84 points (-3.48%) due to late-week profit-taking following a Tuesday peak of 52,374, capping off a highly dynamic week across the continent’s major financial hubs.

Global commodities traded reactively; gold and crude oil markets were driven primarily by shifting geopolitical developments in the Middle East and macro expectations. Gold fell from approximately $4,330/oz to a low of $4,080/oz before recovering to $4,219/oz, marking a second consecutive weekly decline as easing expectations of a prolonged Iran-related supply shock reduced safe-haven demand, while stronger US macroeconomic data reinforced expectations of tighter monetary policy. Meanwhile, oil experienced heightened volatility as fears of supply disruption initially pushed WTI above $95/bbl. and Brent above $98/bbl., before prices retreated sharply to $84.42/bbl. (WTI) and $87.10/bbl. (Brent) by June 12 on optimism around a potential US–Iran peace agreement, possible reopening of the Strait of Hormuz, and prospects for easing sanctions on Iranian oil exports. Despite ongoing regional tensions and intermittent disruptions to shipping flows, improving diplomatic sentiment, higher tanker activity, OPEC+’s planned 188,000 bpd July production increase, weaker Chinese crude imports, and resilient global supply conditions prevented a sustained energy price spike.

The new week is poised for crucial events from the May 2026 inflation report to the NTB auction with an offer of ₦1trn, which is key for market direction, continued preference for long-day bills as the CBN sustains liquidity management through OMO operations, keeping bond yields volatile and T-bill demand on defensive positioning. Equities are likely to mirror cautious positioning, while FX stability persists, supported by improved reserves and steady inflows, despite external risks from volatile energy prices. Anticipatedliquidity inflows of over₦1.26trn, comprising ₦9.10bn FGN 11.20% Jun 2027 Sukuk Bond coupon, ₦206.86bn,and ₦1.26trn in maturing NTB and OMO maturities, respectively, all of which are anticipated to influence investors’ positioning.

In addition to the US FOMC meeting decision, set to be released during the week, worth noting is the fact that this decision serves as a yardstick to the global market.

Subscribe now to keep reading and get access to the full archive.